Ahead Today

G3: US initial jobless claims

Asia: China CPI and PPI, BNM meeting, Taiwan exports

Market Highlights

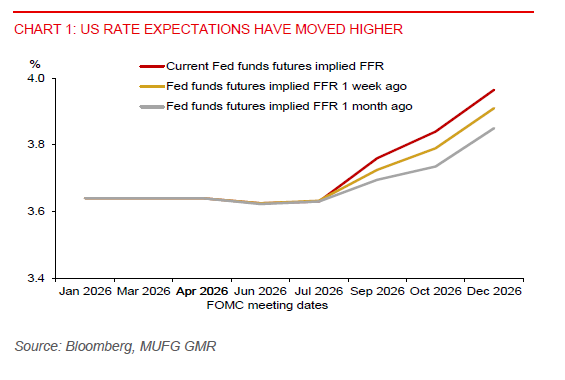

The minutes from the June FOMC meeting highlighted growing concern among policymakers that inflation could remain elevated, even as downside risks to the labour market have moderated somewhat. While members ultimately supported leaving rates unchanged, a few participants noted that there was a case for a rate hike at the June meeting. Policymakers also discussed a range of economic scenarios for the months ahead. In the scenario where inflation remains persistent, most participants indicated that a restrictive policy stance would likely need to be maintained.

Meanwhile, geopolitical risks in the Middle East have resurfaced. US President Trump stated that the ceasefire with Iran has ended, and renewed strikes were launched in response to Iranian attacks on vessels transiting the Strait of Hormuz. Iran reportedly signalled that retaliatory strikes against US bases in the Gulf region are being considered. Brent crude rose another 5% to USD78/bbl yesterday, following a 3% gain the previous day. US Treasury yields also moved higher, with the 2-year yield rising above 4.2% and the 10-year yield increasing 3bps to around 4.58%.

Most Asian currencies weakened further against the US dollar yesterday, led by the INR (-0.6%) and THB (-0.5%). The Thai baht remains particularly vulnerable to higher oil prices and rising US yields, partly due to its relatively low carry profile. As such, the near-term bias remains for further USD/THB upside. In contrast, the KRW outperformed, gaining 0.7%, after policymakers suggested that recent won weakness should prove temporary.

BNM will announce its policy decision today, and we expect the policy rate to remain unchanged at 2.75% as inflation stays contained and growth remains resilient. Meanwhile, Malaysia's trade surplus widened to RM40.4bn in May from RM29.2bn in April, supported by strong electronics and palm oil exports.