Ahead Today

G3: US Dallas Manufacturing

Asia: China Industrial Profits, Singapore Industrial Production

Market Highlights

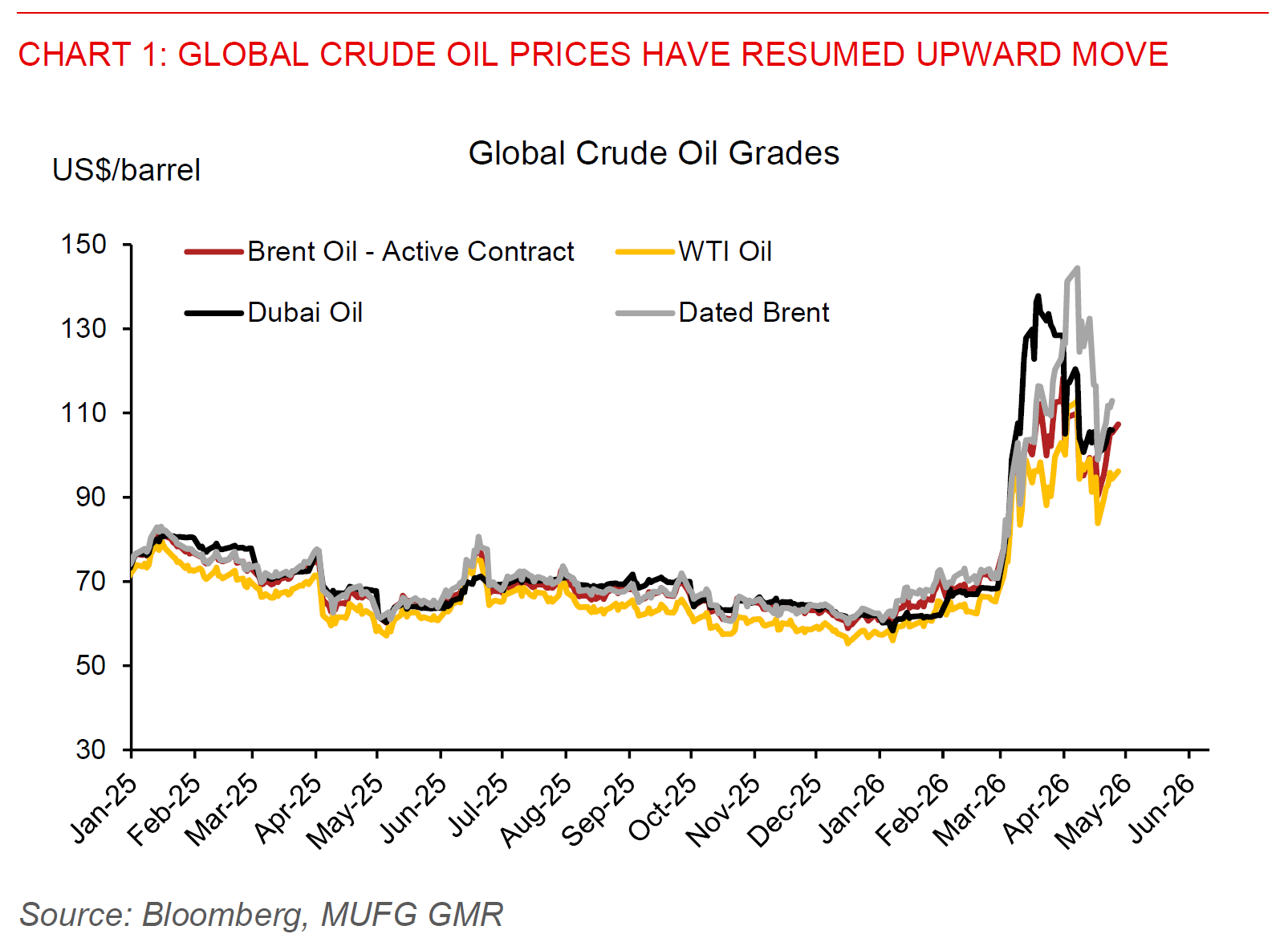

Financial markets, FX and risk assets traded in a mixed fashion, while Brent oil prices rose further above US$100/bbl, as markets tried to digest continued uncertainty around the Iran conflict but coupled with other factors including the strong AI build-out. In particular, President Trump on Saturday told Jared Kushner and Steve Witkoff to skip the trip to Pakistan, and later told reporters that Iran “offered a lot, but not enough”. Iranian Foreign Minister Abbas Araghchi met mediators in Pakistan on Saturday and left Islamabad well ahead of the planned arrival fo the US envoys. Among other things, he said in a social media post that Iran has “yet to see if the US is truly serious about diplomacy”, and that Iran will not enter “imposed negotiations under threats of blockade”. With continued uncertainty around how the Iran conflict will play out, markets are likely to stay on the backfoot for now. Nonetheless, we take recent signs as a positive, both because the US President beyond the words that he uses seems far more likely now to have quite a high bar to further military action, and on the Iran side that there seems to be continued attempts to negotiate including through regional mediators even as the internal political dynamics have of course fundamentally changed.

Our base case is as such for a de-escalation in the Iran conflict moving forward, but of course the longer this crisis drags on the bigger the impact and more salient the demand destruction and inflation impact will be on Asia-ex-Japan.

The good news for Asia is that the AI build-out globally remains very strong and if anything seems to be accelerating, with Intel reporting better than expected results. Last week there were also no less than four new AI models released, including Deepseek’s V4 Preview which were partly trained on Huawei’s Ascent chips and also the likes of ChatGPT’s 5.5, Kimi 2.6, and Tencent’s Hy3 Preview.

This week will be a meaningful week for global central banks, including Bank of Japan on Tuesday, the Fed and Bank of Canada on Wednesday, and the ECB and Bank of England on Thursday. For Bank of Japan in particular it is quite a close call, but latest indications including from news reports suggest the BOJ might be tilting towards a rate hold for now, given the uncertainty around the growth impact of the Middle East conflict. Meanwhile, while the Fed is expected to keep rates on hold, the key for markets is also the shape and policy focus of the Fed under Kevin Warsh as chair, including his desire to reduce the size of the Fed’s balance sheet. Senator Thom Tillis said he is dropping his blockade of Kevin Warsh’s nomination to head the Fed, saying the Justice Department’s decision to end a criminal targeting Fed Chair Jerome Powell removed a threat to the Fed’s independence, and sets the stage for Warsh’ swift confirmation to succeed Powell. Time will tell whether Kevin Warsh is truly as dovish as his public comments suggest, but our sense on the balance sheet issue is that it will likely require broader institutional and financial reforms including on regulation before the Fed’s balance can be meaningfully reduced over time.