Ahead Today

G3: US PPI, empire manufacturing index; Japan tertiary industry index

Asia: China activity data and Q2 GDP

Market Highlights

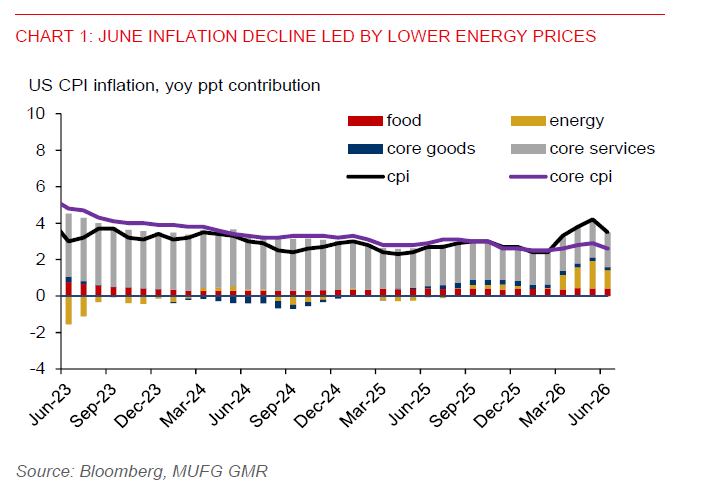

US inflation surprised to the downside in June, with headline CPI easing to 3.5%yoy from 4.2%yoy and below the 3.8% market consensus, largely reflecting lower energy prices. Core CPI also softened more than expected to 2.6%yoy from 2.9%yoy, while monthly core inflation was flat. The softer inflation print prompted markets to largely unwind July hike pricing and scale back some expectations for Fed tightening this year. But markets are still pricing in 1 Fed rate hike by year-end, while Fed Chair Kevin Warsh reiterated that the Fed would not tolerate high inflation.

For FX markets, the key takeaway is that softer inflation has reduced upside risks to US yields, but has not fundamentally altered the high US real yield backdrop. The US dollar index (DXY) softened by 0.3%. USDJPY ended 0.1% lower after recovering from an intraday decline of around 0.5% following the CPI data. In rates markets, the move was led by the front end, with the US 2-year yield falling around 9bps to 4.19%, while the 10-year yield declined around 3bps. Importantly, elevated US real yields continue to provide near-term support for the dollar, while rising geopolitical tensions in the Middle East are likely reinforcing safe-haven demand.

Within Asia, higher oil prices and escalating geopolitical risks continue to create headwinds for the region's net energy importers. INR (-0.6%) and THB (-0.5%) underperformed yesterday, with USDINR moving above 96.00 and USDTHB testing 33.50. Among ASEAN FX, we remain relatively cautious on THB amid renewed oil price risks and heightened Middle East tensions.

Against this backdrop, USDSGD also softened alongside the broader decline in the dollar, helped by a roughly 14bp narrowing in the US-SGD 1-year swap differential. Singapore resilient domestic macro fundamentals remain supportive for the currency. Advance estimates showed Q2 GDP growth of 5.7%yoy, moderating from 6.3%yoy in Q1 but remaining robust, underpinned by continued strength in electronics exports. We continue to view SGD as one of the more defensive Asian currencies.

Meanwhile, a potentially more hawkish Bank of Korea at the meeting this week, continued semiconductor sector strength, and cheap KRW valuations have partly helped the currency to outperform regional peers in recent sessions. KRW appreciated around 0.5% against the dollar yesterday, extending its recent gains.

Elsewhere, China's external sector remained a bright spot. Exports surged 27%yoy in USD terms in June, accelerating from 19.4%yoy in May and exceeding market expectations. Strength was particularly evident in high-tech exports. But growth remains uneven, with domestic demand remaining soft.

A key event risk for Asia FX is China's Q2 GDP release. Market consensus expects growth to slow to 4.5%yoy from 5.0%yoy in Q1. For investors, the implication is straightforward: a weaker-than-expected GDP print would reinforce concerns over domestic demand and likely weigh on regional growth sentiment, supporting a more defensive stance in Asia FX.