Ahead Today

G3: US PCE inflation, initial jobless claims, durable goods orders, new home sales

Asia: BOK meeting, HK exports

Market Highlights

US front-end yields have eased, with the 2-year Treasury yield retracing to 4.03% after touching a high of 4.14% on 22 May. This pullback is notable, where any further follow-through could mark the beginning of a broader downward shift in front-end rates. Markets are still pricing in roughly a 60% probability of a Fed rate hike this year. While this risk of policy tightening cannot be dismissed, particularly against the backdrop of firmer US gasoline prices, a more dovish Fed Chair than currently anticipated could act as a catalyst for yields to move lower. Importantly, underlying inflation appears well anchored, with the trimmed mean PCE running at around 2.2% on a 6-month annualized basis, close to the Fed’s target.

In energy markets, Brent crude has broken lower to $94.29/bbl, falling below the 7 May low of $96.03/bbl. This move likely reflects growing optimism around a potential US-Iran deal. However, there remains uncertainty of an imminent breakthrough. Reports suggest that Trump was “not satisfied” with the progress of negotiations with Iran, while tanker traffic through the Strait of Hormuz is still quite subdued.

The Indonesian rupiah has been one of the worst-performing currencies in the region over the past week. Macro fundamentals continue to drive the weakness, including a widening current account deficit, rising fiscal risks, and deteriorating sentiment towards policymaking, particularly amid plans for greater government control over selected commodity exports.

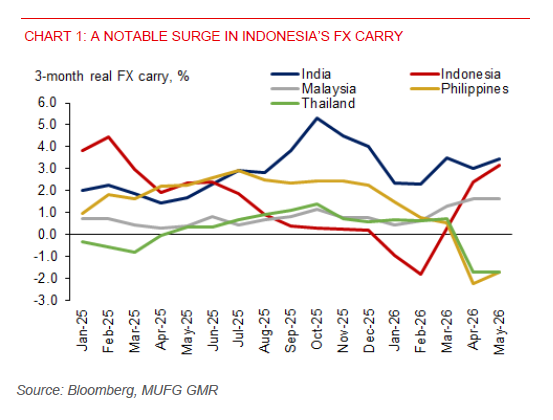

While policymakers are set to discuss the state finance bill, there are no indications yet of any changes to the 3% of GDP budget deficit cap. Policy response is becoming more supportive at the margin. Following the jumbo 50bp BI rate hike in May and a normalization in inflation in April, Indonesia’s 3-month FX carry has risen notably, reflecting Bank Indonesia’s efforts to enhance the rupiah’s attractiveness (see chart 1). At the same time, from a technical and valuation perspective, risks of a reversal in USDIDR are beginning to build.

Elsewhere, the key focus today is the Bank of Korea (BoK) policy decision. We expect the BoK to remain on hold, broadly in line with market expectations. However, the risk is skewed towards a hawkish hold, given inflation remains above the 2% target. Any firm inflation narrative from the Governor could offer some near-term support to the Korean won, which has been under pressure amid persistent foreign equity outflows.