Ahead Today

G3: US NY Fed 1y inflation expectation

Asia: Indonesia foreign reserves

Market Highlights

The US dollar gained around 0.7% to test the 100.00 psychological level following a stronger-than-expected nonfarm payrolls report. Markets have moved to fully price in one 25bp Fed rate hike by end-2026, while the US 2-year yield rose by around 10bps. Headline payrolls increased by 172k in May, nearly double the market consensus of 88k, while the unemployment rate held steady at 4.3%, reflecting still-resilient labour market conditions. Near-term US rate cuts are effectively off the table, with the strength of the employment report providing a supportive backdrop for a firmer dollar, which strengthened against both G10 and most emerging market currencies.

While Brent crude and US gasoline prices have eased in recent weeks, they remain relatively elevated, suggesting that upcoming US CPI could still print above 4%yoy in May, up from 3.8%yoy in April. This would likely keep US rate expectations biased higher-for-longer, underpinning USD strength, particularly as the US-Iran conflict still shows no clear signs of resolution. That said, US wage growth has moderated to around 3.4%yoy in May, which could partially offset energy-driven inflation pressures at the margin.

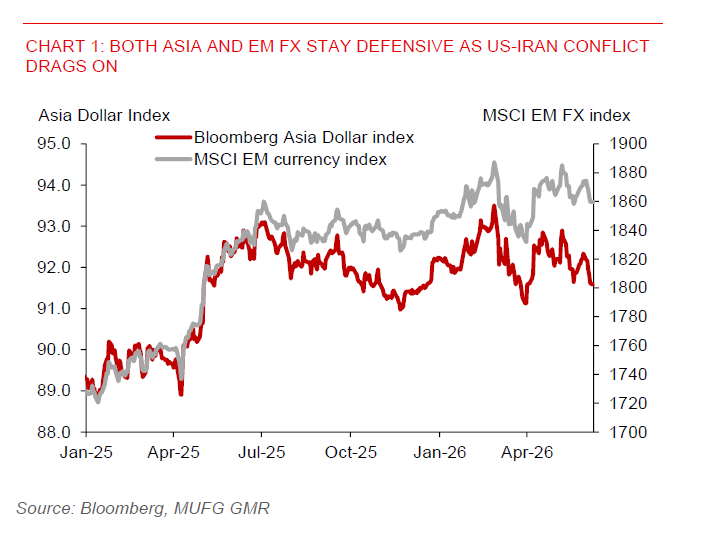

In Asia, currency performance continues to reflect a combination of a stronger dollar, higher US yields, and macro headwinds from elevated energy prices, particularly for economies running current account deficits such as INR, IDR, and PHP. Stronger US yields are also weighing on KRW, where real rates have turned increasingly unattractive, exacerbating capital outflow pressures. By contrast, policy-anchored currencies such as CNY have remained relatively resilient. While SGD’s resilience is similarly underpinned by MAS’s S$NEER-based policy framework, USDSGD remains highly sensitive to shifts in US front-end yields. In the absence of any near-term resolution to the US-Iran conflict, higher-than-expected US yields suggest that our bias for USDSGD has shifted modestly to the upside, although we expect any gains to be relatively contained.

The Indian rupee has been a notable exception, strengthening against the dollar last Friday on the back of targeted policy support from the RBI. While the central bank kept its policy rate unchanged at 5.25%, it introduced measures aimed at attracting capital inflows and stabilizing the currency. Notably, the RBI will absorb hedging costs for banks raising 3–5 year foreign currency non-resident (FCNR) deposits until end-September. This effectively allows banks to offer higher returns, potentially by 100–200bps, to attract USD inflows, providing near-term support for the rupee.

In Indonesia, authorities have also stepped up efforts to attract inflows, including raising yields on SRBI instruments and signalling a willingness to raise yields on local assets. However, persistent investor concerns around institutional quality, fiscal risks, and equity investability have continued to drive net outflows from both equities and bonds, weighing on the rupiah. Liquidity conditions in the USD/IDR market remain tight, reinforcing a bias toward further rupiah depreciation. For now, there is little in the way of a clear catalyst to reverse the ongoing “triple selling” dynamic across local equities, bonds, and the currency.