Ahead Today

G3: US personal income, initial jobless claims, PCE inflation, Q1 GDP, leading index; eurozone CPI and Q1 GDP, ECB policy rate decision

Asia: Philippines trade data, China PMI, Singapore unemployment rate, Thailand bop, Taiwan Q1 GDP

Market Highlights

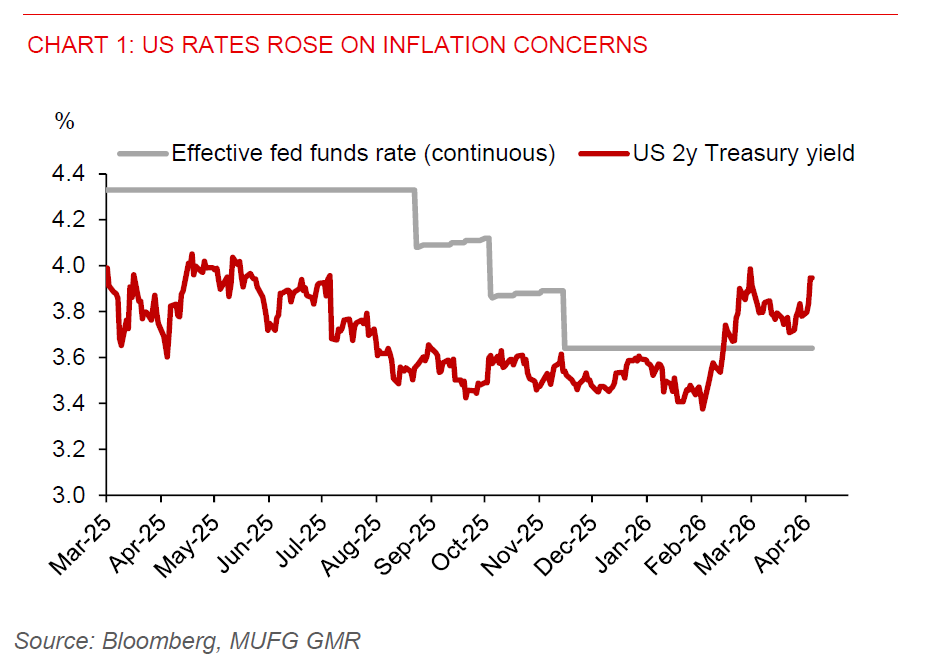

Brent crude surged to around US$120/bbl, supporting USD strength, after President Trump reportedly rejected Iran’s proposal to reopen the Strait of Hormuz. The US dollar remained supported in the 98.00–99.00 range, underpinned by a further rise in US yields that has reinforced the carry appeal of the dollar. The US 2-year yield climbed around 11bp to 3.95%, while the 10-year yield rose roughly 8bp to 4.43%.

Fed messaging has further reinforced this hawkish repricing of rates. While policy rates were left unchanged as widely expected, dissent from three committee members against signalling an easing bias in policy statement highlights growing unease over inflation risks. Chair Powell’s decision to remain on the Fed’s Board of Governors after his Chair term ends in May also removes the immediate scope for President Trump to reshape the Board. At the same time, Trump’s preferred Fed Chair candidate, Kevin Warsh, cleared a key Senate hurdle to replace Powell.

From a macro perspective, today’s US PCE inflation release could keep the dollar firm. US gasoline prices have surged to around US$4.84/gallon from pre conflict levels near US$3.50, adding to near term inflation pressures. With markets looking for March PCE inflation to rise to around 3.5%yoy from 2.8% previously, the risk skew remains toward a hawkish repricing of US rates, keeping dollar supported in the near term.

Asian currencies weakened against the dollar, with losses led by KRW (-1.1%), THB (-0.6%), and PHP (-0.5%) as oil prices continue to trade higher. With US and Iran locked in a prolonged standoff, the continued disruption to energy flows through the Strait of Hormuz are pushing up oil prices, adding downward pressure on oil-sensitive regional currencies. PHP and THB will remain vulnerable, given their high correlation with oil prices, while unfavourable fiscal-energy dynamics for Indonesia continues to weaken the rupiah. More credible signs of de-escalation are needed to ease depreciation pressures.

USDCNH rebounded to 6.84-6.85 level, after nearly falling to the 6.80 level. The PBOC has set broadly steady USDCNY fixings since mid April, signalling a preference for near term stability in the yuan following roughly a year of broad appreciation.

USDTHB rose to around 32.70, retesting the 32.50–33.00 range. The baht’s weakness reflects Thailand’s high reliance on crude imports, with roughly 60% sourced from the Middle East. The Bank of Thailand kept its policy rate unchanged at 1%, in line with expectations, while flagging a slowdown in growth to 1.5% this year from 2.4% in 2025. Headline inflation is projected to average 2.9% this year, compared with -0.1%yoy in March, implying a further erosion of real rates and weighing on THB’s relative appeal.