Ahead Today

G3: Eurozone Consumer Confidence, Fed’s Waller remarks

Asia: China Loan Prime rate

Market Highlights

The US and Iran began talks in Switzerland on a peace deal to settle Iran’s nuclear program, even as continued risks of a reignition of the conflict between Israel and Lebanon threatened to halt the deal. Developments over the weekend were confusing, with Iranian media reporting that Iran halted talks over Trump’s latest threats, and Trump saying in social media posts that he would strike Iran again if it does not immediately stop Hezbollah in Lebanon from causing trouble.

Overall, while oil prices rose on these developments and this weighed on sentiment somewhat, the overall level of oil prices seem to be low enough to support risk sentiment. Beyond the Iran conflict, the key driver of Asia FX and rates markets is also the changing nature of the Fed under new Fed Chair Kevin Warsh, and the spillover from both a stronger Dollar and also sticky US yields. As such, while the previous underperformers such as INR and PHP have been more resilient in the near-term due to lower oil prices, we have seen some underperformance in the low yielders in our region as the drivers shift towards rate differentials.

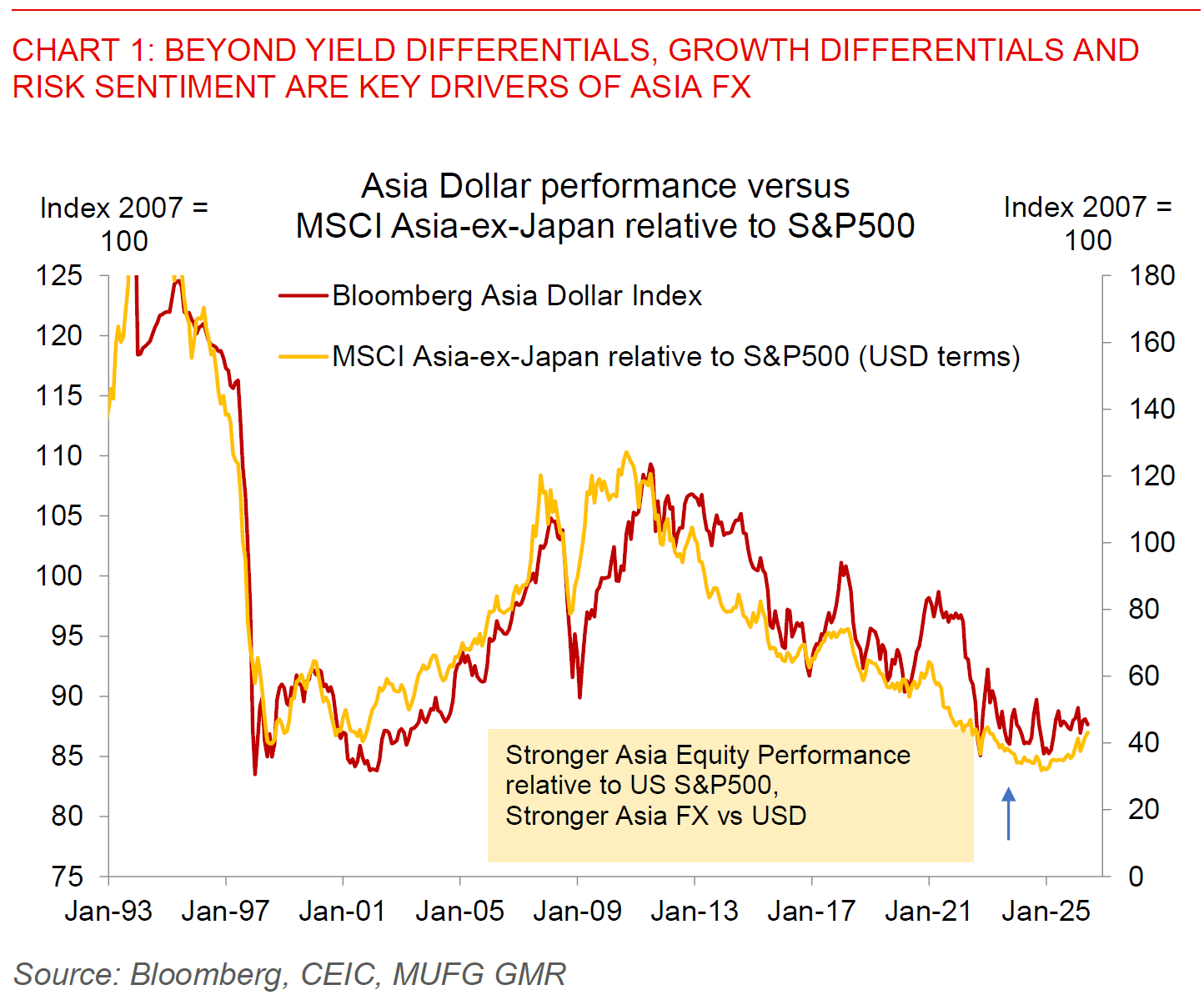

Moving forward, our base case for Asian currencies is that they will also receive support from better growth differentials with the US, especially the likes of AI electronic exporting currencies such as South Korea, Taiwan, Malaysia, and Singapore. Our previous framework on the drivers of Asia FX analysing past Fed rate cycles shows that yield differentials is only one factor influencing currencies in our region, with growth differentials and risk sentiment just as importantly if not sometimes more important (see Asia FX – the impact of Fed’s easing cycle and more). Of course, if the Fed does turn materially more hawkish and this also results in declines in risk appetite in markets this will certainly matter for Asia FX. But if our base case holds, overall strong growth in Asia, decent improvement in risk sentiment should be able to more than offset what we have seen and expect to see from the Fed moving forward.

Of course, not all things are global in nature and there are also local drivers of currencies, and most pertinently for the current account deficit currencies in our region which are dependent on external funding. In Indonesia in particular latest news suggests that the Attorney-General Office (AGO) has begun seizing thousands of electric motorcycles procured by the National Nutrition Agency (BGN) as part of a massive corruption investigation linked to the government’s free nutritious meal programme. The key for markets and the Indonesian Rupiah beyond the political noise is whether this will result in more fiscal discipline by the Indonesia government both directly on budget and also off-budget indirectly through below the line item spending and also contingent liabilities. For now we are not that sanguine that it will fundamentally change the nature of spending programs and as such remain cautious on IDR, but this would be key to monitor moving forward.