Ahead Today

G3: Trump-Xi Summit Day 2

Asia: Malaysia GDP, India Trade Balance

Market Highlights

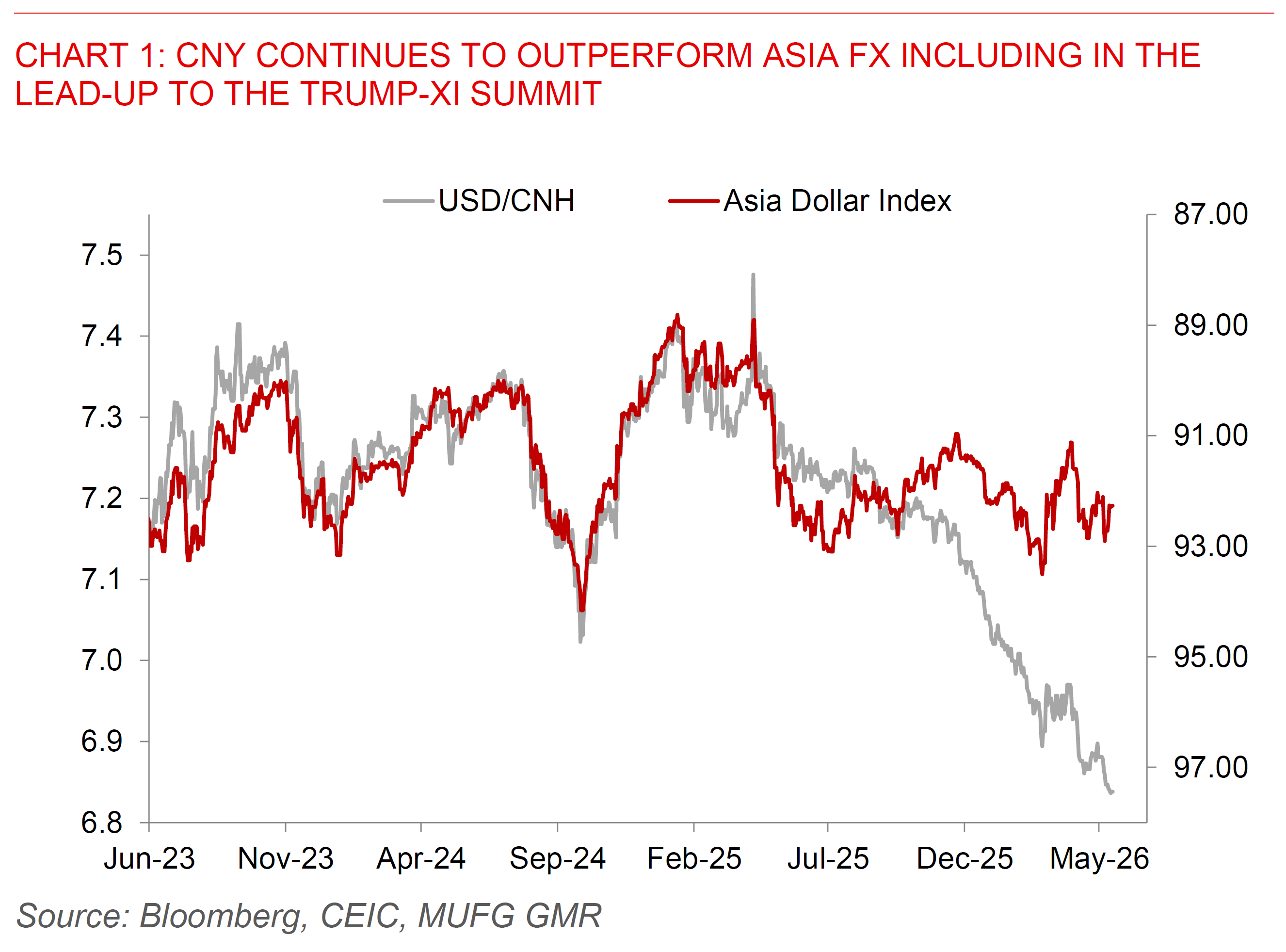

The first day of the Trump-Xi summit in Beijing on 14 May struck a broadly constructive tone, though produced no comprehensive trade deal. Trump arrived flanked by over a dozen top US CEOs — including Elon Musk, Jensen Huang, Tim Cook and Jane Fraser — underscoring the commercial focus of the visit. The two leaders held a two-and-a-half-hour closed-door meeting at the Great Hall of the People, with Xi calling for a "constructive, strategic and stable" relationship and Trump expressing hope that ties would be "stronger and better than ever before." The most tangible deliverable was China's commitment to purchase approximately 200 large Boeing aircraft, alongside an invitation for Xi to visit the White House in September. On Iran, Trump said Xi indicated China wants to help negotiate an end to the conflict and supports reopening the Strait of Hormuz. The summit's sharpest moment came, when Xi warned that mishandling the Taiwan issue could lead to "clashes" between the two superpowers. Day Two today is expected to focus on whether the two sides can formalise a trade dispute mechanism, provide clarity on agricultural purchases following a confusing reversal on US beef licenses, and address technology and chip access.

Nvidia's chip exports to China remains a live issue after Reuters reported that the US Commerce Department has approved around ten Chinese companies, including Alibaba, Tencent, ByteDance and JD.com, to purchase Nvidia H200 AI chips, with each approved buyer permitted to acquire up to 75,000 units either directly from Nvidia or through intermediaries such as Lenovo and Foxconn. The actual status is unclear, but what’s notable as well is the immediate market reaction, with China stocks especially tech counters dropping while in contrast those in the US rising. US equities hit fresh records, with the S&P 500 rising 0.8% to close above 7,500 for the first time, the Nasdaq Composite gaining 0.9% to 26,635, and the Dow Jones crossing 50,000 for the first time since the Iran war began. The rally was driven by Cisco Systems — up ~13% on a strong AI-focused outlook — Cerebras Systems surging nearly 70% on its IPO debut, and Nvidia extending its winning streak to seven sessions with its market cap approaching $6 trillion. Chinese mainland markets moved in the opposite direction: the Shanghai Composite fell 1.5% and the CSI 300 dropped 1.7%, consistent with the observed pattern of Chinese stocks rallying into a Trump-Xi meeting and selling off after, as the summit is priced as a stabilisation exercise rather than a structural catalyst. On FX, the dollar gained approximately 0.3% — its largest single-day advance since 29 April — supported by stronger-than-expected US retail sales, weighing on most EM currencies and pushing gold lower as haven demand faded.

India produced a cluster of significant policy moves this week, all tied to the government's austerity push amid the Strait of Hormuz driven pressure on capital flows and balance of payments. The Finance Ministry raised import duties on gold and silver to 15% from 6%, effective 13 May, and on Thursday capped duty-free gold imports under the Advance Authorisation scheme at 100 kg per approval — measures aimed at curbing non-essential imports and supporting the rupee which continued to hit record lows. On the work-from-home front, Delhi government offices announced staff will work from home twice a week as part of the city's austerity plan, following PM Modi's broader public appeal to reduce fuel consumption. Separately, Bloomberg News reported that India is considering a significant reduction in withholding taxes paid by foreign investors on domestic bonds, a move recommended by the RBI to the Finance Ministry. Overall we continue to remain cautious on INR and think that even in a de-escalation base case, we see INR underperforming key G10 and Asian currencies.