Ahead Today

G3: US ISM Services, US New Home Sales, US JOLTS Jobs Opening

Asia: Reserve Bank of Australia, Indonesia GDP, Singapore Retail Sales, Philippines Inflation

Market Highlights

Brent oil prices spiked to US$114/bbl, risk assets sold off and the Dollar strengthened, as the worst escalation since the ceasefire resulted in renewed concerns around the US-Iran conflict. It’s unclear what the first trigger was, but among other things President Trump’s announcement of “Project Freedom” to guide ships out of the Strait of Hormuz was followed by Iranian officials announcing that any US attempt to interfere in the Strait of Hormuz would be a breach of the ceasefire. While there have been conflicting reports since, what we do know is that there were missiles targeted at the UAE and in particular energy installations in UAE’s Fujairah, coupled with claims of downing of Iranian “fast” boats by the US military, unconfirmed strikes on a US military ship, coupled with damages on a South Korea cargo ship.

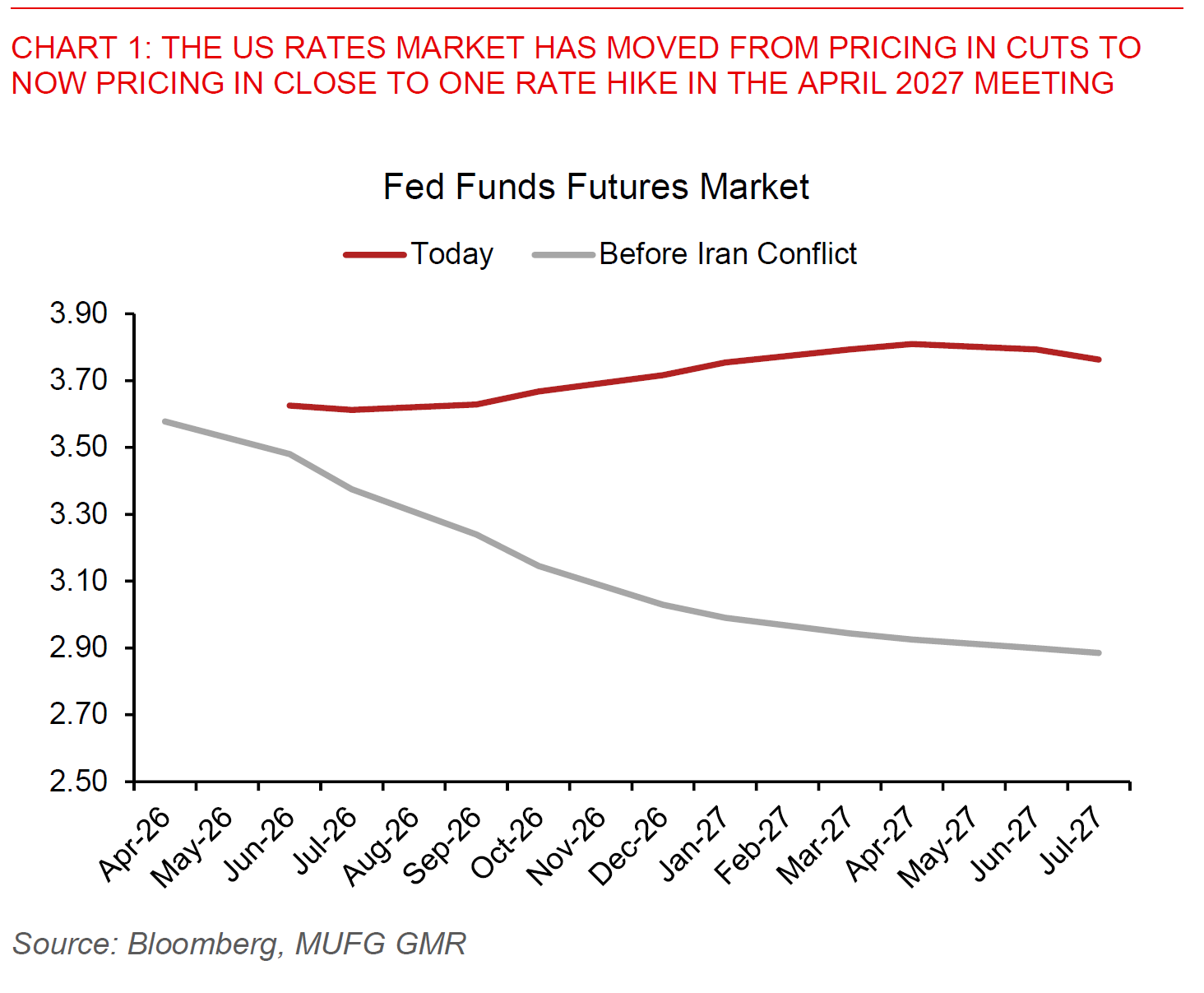

What’s interesting as well is that the US rates market has now moved from pricing in no cuts, to now pricing in close to one Fed rate hike one year ahead into April 2027, across both the Futures and OIS markets. This comes as new Fed Chair Warsh is inheriting a far more divided FOMC with three dissents in the last meeting in April against inclusion of guidance of rate cuts.

Overall, the key message from us is that the starting point matters for the impact to each currency including in Asia, beyond just the direct sensitivity of the Strait of Hormuz and linkages to oil prices and energy shortages.

First, for those markets which were already starting out with the economy running above trend, and with that some earlier concerns around inflation, the chances of central bank rate hikes are as such far likelier. On this front, Australia is one key example of a market in this bucket. We have the Reserve Bank of Australia meeting later today, and the market is already pricing in 19bps of rate hike in this meeting, coupled with 65bps of rate increases over the next 9 months. With capacity constraints, low productivity and sticky inflation a key concern for the RBA, the communication by Governor Bullock in terms of path moving forward will be closely watched for moving forward. We are biased to think that the RBA will probably deliver fewer rate hikes than are currently priced in the markets, and from a FX perspective what would matter for AUD/USD is also whether risk sentiment holds up moving forward.

Second, the starting point matters in terms of the linkages to the AI boom, which we believe is a structural megatrend and we are likely only in the early innings of a multi-year investment boom which will help Asian exporters as well. On this front, we had the Bank of Korea’s Senior Deputy Governor Ryoo Sangdai saying yesterday that the BOK likely needs to consider raising interest rates given prices are rising faster than expected. With South Korea’s exports improving meaningfully including through higher DRAM prices and helped by the memory cycle, the bias and risk for policy rates in Korea would tilt towards being higher rather than lower.

Third, the starting point on FX and capital outflows. On this front, the likes of the Indian Rupee and to a smaller extent Vietnam Dong were already facing strong capital outflows to begin the Iran conflict, and our continued bias is to as such see INR underperform across a range and distributions of scenarios. We had news reports from Reuters yesterday that the RBI is considering measures to attract more Dollar inflows, and among other steps the 2013 FCNR swap scheme coupled with elimination of withholding tax on overseas government bond investors are possible ways to support the Indian Rupee. We see USD/INR trading between the 95.00 to 96.00 over the next 12 months, implying continued FX underperformance.