Ahead Today

G3: US Empire Manufacturing

Asia: India WPI, Philippines Remittances

Market Highlights

The US and Iran are looking to arrange a second round of peace talks in the coming days, with President Trump saying the objective is to hold more discussions before a 7 April ceasefire expires next week, according to new reports. In particular, Trump said talks could resume “over the next two days” in Pakistan, the New York Post reported. That would build on a marathon yet inconclusive session in Islamabad over the weekend, while Trump reiterated he sees the war as “close to over” in a Fox Business interview. At the same time the US administration is enforcing a blockade on Iranian ships from the Strait of Hormuz, and according to the US six merchant vessels complied with instructions from its forces to turn around and re-enter an Iranian port during the first day of blockade. Reports also suggest that the Iranians have been taking a more measured strategy in its response in the near-term to keep talks and negotiations going with the US administration, although this is not to say that it will not change moving forward.

From a financial market perspective, it’s amazing how much has retracted in terms of the negative hit to risk sentiment post the Iran conflict, and in particular the US Dollar has also pretty much weakened beyond the pre-conflict levels as we speak. Asian currencies have also been helped by the weaker Dollar trend but over in our region we note greater dispersion in outcomes across currencies. Our existing currency preference favouring the likes of CNY and MYR, and seeing underperformance in the likes of INR, VND and PHP continues to play out, even as the exact FX levels will be dependent on global factors as well.

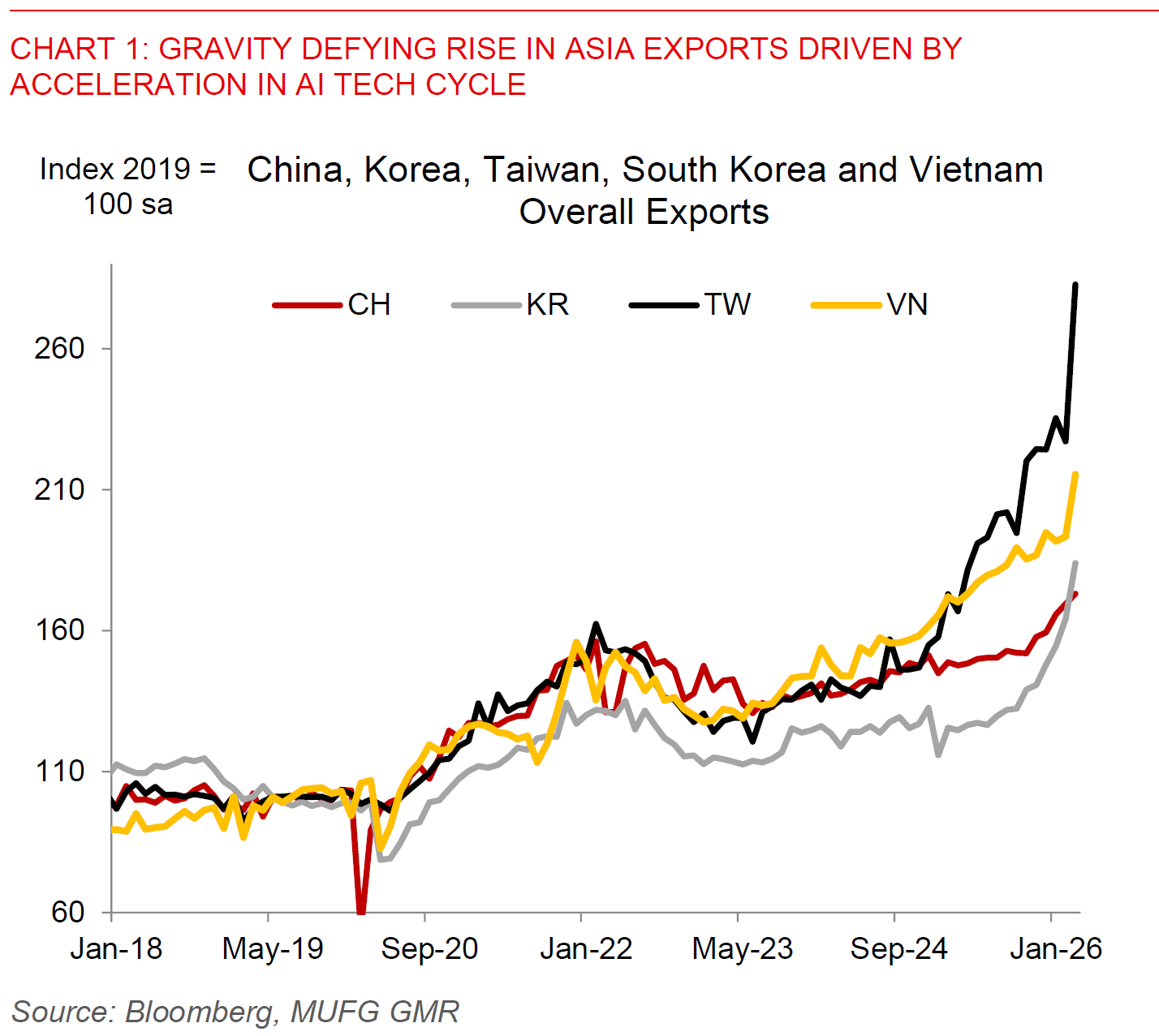

It’s also important to remember the starting point of our region and each country. And the starting point is that Asia entered into this conflict with very strong export momentum helped by the continued acceleration in the AI and technology boom. The early export reporters across our region such as Taiwan, South Korea, and Vietnam have seen a meaningful pick-up in the pace of export momentum especially in March, while in China’s case even though year-on-year changes in exports moderated meaningfully we think this was due more to seasonal timings rather than a slowdown. South Korea also just released export price data showing a sharp 28%yoy rise for March and likely reflecting a strong acceleration in DRAM prices.

In South Korea’s case, while it’s definitely hurt in a scenario of prolonged conflict and higher oil prices, our base case forecasts in a de-escalation scenario has KRW outperforming to some extent in part due to our expectation for the strong AI and tech cycle to continue notwithstanding risks from oil prices and energy supplies. Beyond the fundamentals, South Korea’s NPS is scrapping a long-standing 15% cap on forex hedging, aiming for greater flexibility during periods of market volatility, according to a statement released yesterday. This 15% level will instead serve as a baseline ratio, with FX hedging now viewed as a core policy in overseas investment rather than applied only in exceptional circumstances. This is a very key change in NPS FX strategy, and with implications not just for the near-term but also potentially over the medium-term.