Ahead Today

G3: US wholesale inventories; Germany and France CPI

Asia: Philippines trade, Thailand BOP, Taiwan Q1 GDP

Market Highlights

The US dollar softened modestly but remains firm for now while front-end US yields continue to ease. In particular, the US 2-year yield has pulled back further, with the intraday high of around 4.14% on 22 May now appearing to cap the upside. The recent decline in front-end yields is notable and could signal the early stages of a broader move lower.

On the macro front, April PCE inflation rose to 3.8%yoy from 3.5% in March, in line with expectations. However, the sequential trend points to some moderation in price pressures, with headline PCE at 0.4%mom, easing from 0.7% previously and coming in slightly below the 0.5% market consensus. Core PCE similarly met expectations at 3.3%yoy, while rising just 0.2%mom, softer than the expected 0.3%mom print. Alongside this, activity indicators also showed signs of cooling. Personal income was flat in April, down sharply from 0.6%mom in March and below the 0.4% consensus, while personal spending slowed to 0.5%mom from 0.9% previously.

Brent prices also closed lower, and technical indicators point to further downside. Reports that the US and Iran have reached a tentative agreement to extend the ceasefire by 60 days, pending approval from President Trump, further support the view that geopolitical risk premia may continue to unwind in the near term.

Across Asia, FX markets remain driven by headline risks, with geopolitical developments continuing to shape near-term sentiment. News of US strikes on Iran weighed on risk appetite yesterday, contributing to heightened volatility across regional currencies. While such developments are likely to keep markets sensitive in the near term, the balance of probabilities still points toward de-escalation, with both the US and Iran appearing incentivized to pursue a diplomatic resolution.

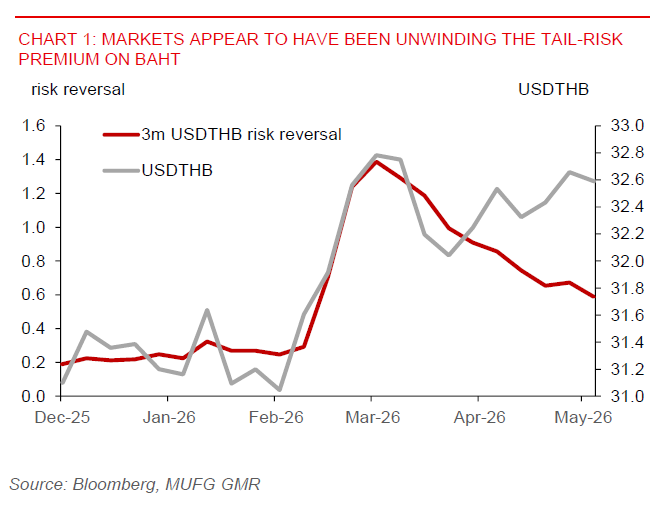

In Thailand, the outlook for USDTHB appears to have turned less bullish, with markets showing signs of unwinding the tail-risk premium that had been priced into the baht during the early phase of the Iran conflict (see chart 1). This shift is consistent with the recent decline in oil prices, as well as Thailand’s efforts to strengthen its oil inventories over recent months, which help reduce external vulnerability.

For the Singapore dollar, while upward momentum in USDSGD has been gradually building recently, we expect the currency to remain relatively resilient against both the US dollar and regional peers. MAS policy continues to provide a strong anchor, with a steeper S$NEER slope, estimated at around 1% per annum, reinforcing an appreciation bias. Moreover, USDSGD volatility has remained contained, and any near-term upside in the pair is likely to be capped by strong technical resistance around the 1.2900 level in our view.