Ahead Today

G3: US CPI, NFIB small business optimism

Asia: India CPI

Market Highlights

Hopes for a swift reopening of the Strait of Hormuz continue to fade. Brent remains above $100/bbl, while conditions in the physical oil market are tightening further. According to Saudi Aramco, each week of disruption at the Strait is removing around 100 million barrels of crude from global supply, underscoring the severity of the energy shock.

Inflation pressures are building as a result, including in the US, where average gasoline prices have stayed elevated above $5 per gallon. US CPI data due later today is therefore likely to print higher than March’s 3.3%.

That said, upside momentum in the dollar should remain constrained. A sharp hawkish repricing of US rates expectations appears unlikely in our view. Even after a stronger-than-consensus April nonfarm payrolls report, the dollar failed to mount a meaningful rally. Against a backdrop of firmer inflation, the Fed is more likely to remain on hold than to resume rate hikes.

In Asia, the Indonesian rupiah remains under pressure, trading above the 17,400 level against the dollar, as lingering energy disruptions raise the risk of fuel shortages. Indonesia’s vulnerability is heightened by relatively low crude inventory buffers, largely due to storage capacity constraints. That said, Indonesia has secured Russian oil supply of up to 150mn barrels, which should help to strengthen its energy supply buffer.

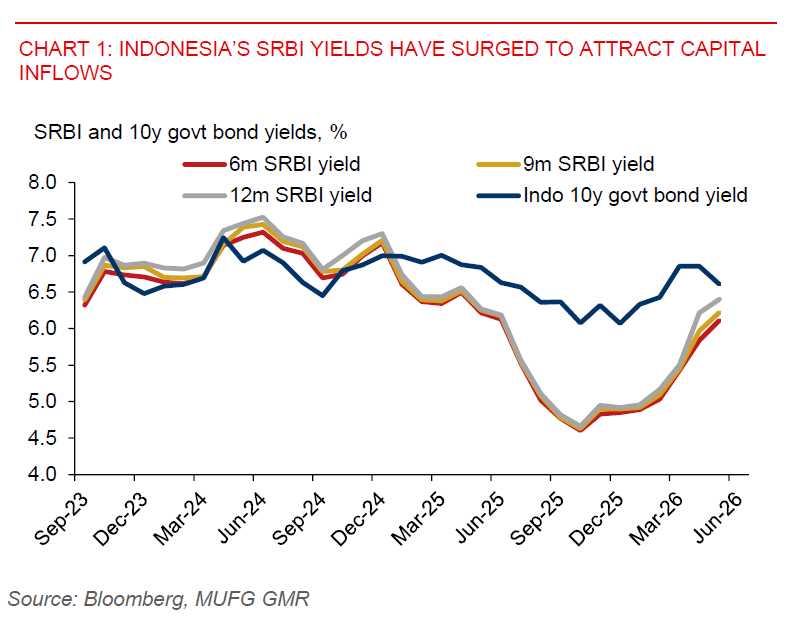

Bank Indonesia (BI) has remained proactive in stabilising the rupiah. Notably, outstanding rupiah bills (SRBI) rose by IDR126.7tn in April to IDR957.9tn, as BI stepped up efforts to attract capital inflows. SRBI yields have also climbed above 6%, reinforcing the carry appeal. Against this backdrop, the probability of a 25bp policy rate hike this month has increased, particularly with Q1 growth printing at a robust 5.6%yoy.

Elsewhere, oil sensitive currencies led regional declines yesterday, with INR (-0.9%), PHP (-0.8%), and THB (-0.7%) underperforming as oil prices remain elevated. KRW also weakened by 0.7%.

India’s April CPI data is due today. Inflation tailwinds are building amid higher energy prices and a softer rupee, raising the risk that the RBI may need to tighten policy further to contain inflation and support the currency. We see upside risks to April CPI relative to the market consensus of 3.8%yoy. If such upside risks materialize, USDINR could register its highest weekly close on record.