Ahead Today

G3: US nonfarm payrolls

Asia: CPI data from Thailand, Philippines, and Taiwan, RBI meeting, India Q1 GDP

Market Highlights

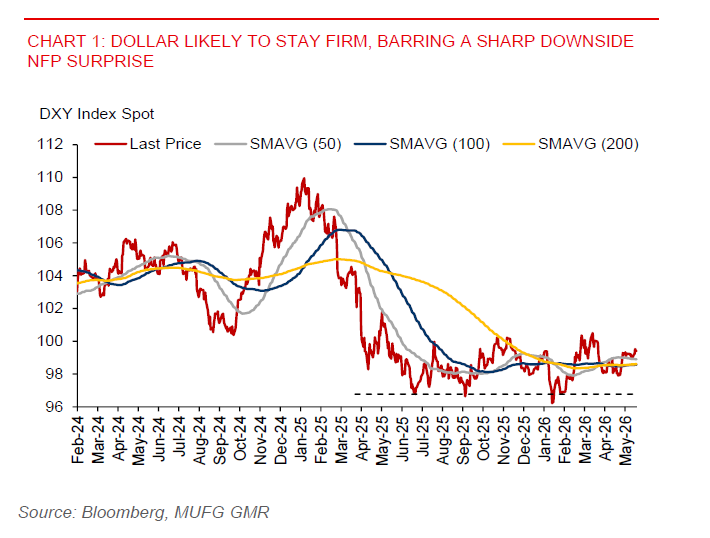

US nonfarm payrolls (NFP) is due later today alongside the unemployment rate and wage growth. DXY remains firm above the 99.00 level, with markets rebuilding net long USD positioning since mid-May after a short period of modest unwinding. Positioning is not particularly stretched, while the dollar itself remains softer than what positioning would suggest.

Following April’s 115k print, the upcoming NFP release could show a moderate slowdown rather than a sharp deterioration. With consensus already soft at 88k, downside risks are broadly priced, leaving the overall risk profile balanced in our view. Initial jobless claims rose to around 215k in on average in May from 208k in April. The ADP employment only improved modestly to +122k in May from +105k in April. Meanwhile, the ISM services employment index was broadly unchanged at 47.9 in May from 48.0 in April.

Given the balanced risk backdrop, a modest in-line or slightly soft print is unlikely to trigger a meaningful hawkish repricing of Fed expectations. The bar for a sustained USD rally on the back of NFP remains high.

Across Asia, currencies continue to trade defensively as progress on a US–Iran peace deal appears to have stalled. Meanwhile, clashes persist in Lebanon, with the Iran-backed Hezbollah group rejecting a US-brokered truce. KRW and IDR led losses against the US dollar yesterday, with the rupiah in particular breaking above the 18,000 level. Further policy tightening is likely needed to stem persistent depreciation and cushion the pass-through of higher energy costs to domestic inflation.

A key focus today is the RBI policy meeting. While consensus expects rates to remain on hold at 5.25%, we see a meaningful risk of a 25bp hike at this meeting, as the central bank looks to manage inflation pressures and shore up the rupee.

The Philippines inflation print will also be closely watched for BSP policy signals. Headline inflation already rose to 7.2% YoY in April, well above target. With oil prices remaining elevated, inflation risks are skewed to the upside, which could reinforce the case for further policy tightening to contain price pressures and support the PHP.