Ahead Today

G3: US Factory orders, US Durable Goods orders

Asia: Indonesia trade, Indonesia Inflation

Market Highlights

President Trump said the US will begin guiding some neutral ships trapped in the Persian Gulf out from the Strait of Hormuz, even as he said that the US is having “very positive discussions” with Iran. With that oil prices remained volatile, even as Brent oil has fallen quite sharply from local peaks of US$122/bbl down to around US$108/bbl at the time of writing. Overall, we are biased to think that further military escalation is quite unlikely based on what we know, and we are inclined to think that Trump is looking for a way that would allow him to claim victory in the Iran conflict, although whether the status quo prolongs or a de-escalation ensues is still unclear at this point in time.

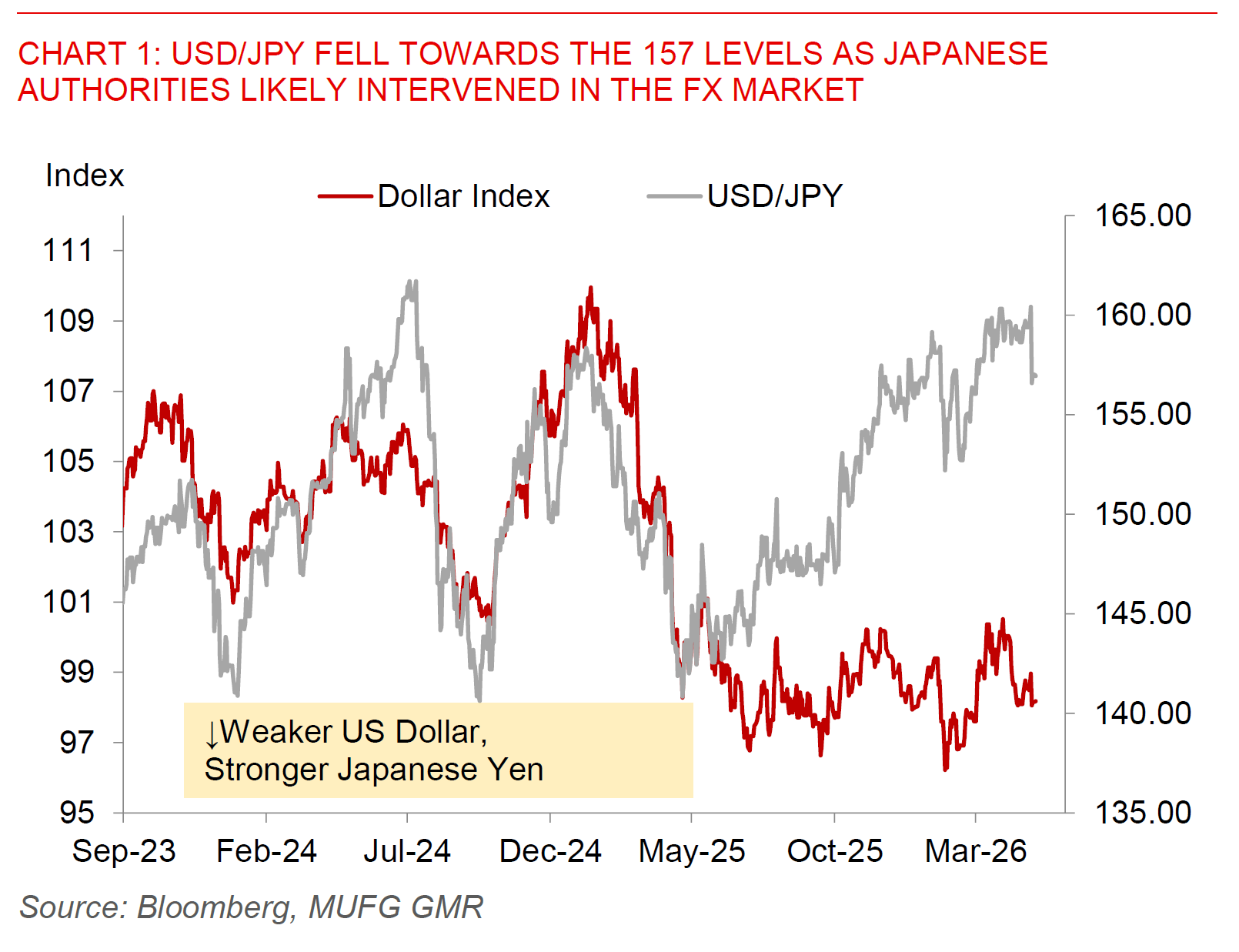

There were three big developments for markets in recent days – 1) FX intervention by Japanese authorities to prop up the Japanese Yen, 2) China’s pushback against the imposition of US sanctions on Chinese refiners and purchases of Iranian oil, and 3) Vietnam’s inclusion as a “priority foreign country” for Intellectual Property protection, which we think might be the US way to push Vietnam to take more action against alleged transshipment and Chinese value added in its manufacturing supply chains.

In particular, USD/JPY fell sharply from a peak of closer to 160 to slightly below 157 at the time of writing, with likely FX intervention on Thursday evening Asia time to help to push down USD/JPY. This likely continued on Friday as well amidst a holiday-shortened week amongst many Asian countries. Estimates by market participants based on current account deposit data released by the Bank of Japan and relative to changes in money market positions showed that intervention could have been around JPY5-6 trillion, or around US$32-38bn. If these preliminary estimates are correct, the magnitude would be quite similar to FX intervention during April 2024 and Oct 2022. Whether these efforts result in a sustainable return in USD/JPY lower would ultimately have to depend also on the fundamentals, and in particular whether the Fed turns more dovish and importantly whether the Bank of Japan deliver on rate hikes moving forward. Our base case remains for two BOJ rate hikes in June and December this year, and this will be a crucial assumption together with de-escalation in the Strait of Hormuz in forecasting a gradual move lower in USD/JPY towards the 152 levels.

Meanwhile, China has for the first time since the passage of its Blocking Statue in 2021 formally invoked it, prohibiting compliance with recent US sanctions targeting five Chinese refineries on the grounds of participation in Iranian oil transactions. As such, third parties which fear and comply with US sanctions may now face Chinese legal risks if they continue to comply with US sanctions. The Blocking Rule is designed as such to change the transmission mechanism of US secondary sanctions, by telling market participants that complying with unjustified US extra-territorial sanctions may not necessarily be the “safe option”. Overall, we think this is a very significant development and is worth watching closely, and not just because it comes ahead of a planned summit between President Xi and Trump. There is a big question around why now, and our hypothesis is that it is both because the announced sanctions hit some major “teapot” refiners in China, and importantly also because China has built up more sources of resilience in payments including in diversification from the US Dollar and financial system that it feels confident enough to invoke the Blocking rule for the first time. Moving forward as such, it seems fair to expect more offensive measures by the Chinese side to protect China’s interest, and especially if this example ultimately showcase China’s ability to push back against the enforcement of US sanctions.