Ahead Today

G3: US NFIB Small Business index, US PPI

Asia: China Exports and Trade

Market Highlights

Trump began a US naval blockade of the Strait of Hormuz, but overall risk assets rebounded with signs that there continues to be talks between US and Iran. In particular, Trump signalled in a press conference yesterday that there were further talks on Monday, and that the “right people… appropriate people” called and that Iran wants to work a deal. Trump claims that the negotiations failed due to Iran’s insistence on maintaining a nuclear program, and that he was sure Iran will eventually agree to abandon nuclear ambitions, and reiterated that there would be no deal without that concession. Overall whether this positive risk sentiment holds in financial markets will partly depend on the extent of enforcement of the current blockade, and whether there is a narrow path towards a deal. We think there are both positives in terms of the progress in negotiations and technical discussions that have already been made, but also meaningful negatives from a potential flare-up in tensions and especially for Asian markets which are highly dependent on the Strait of Hormuz for energy flows.

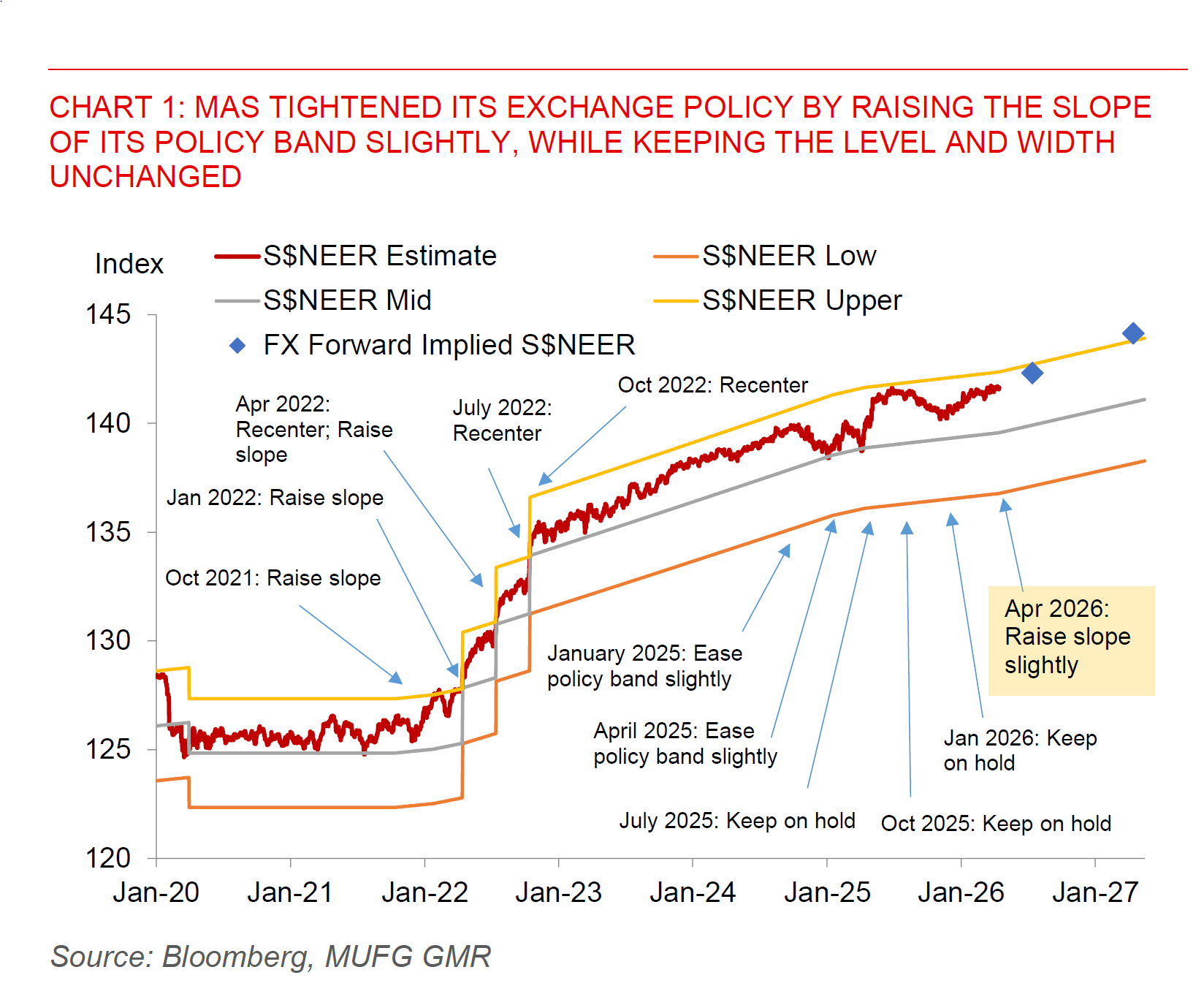

The Singapore central bank tightened its exchange rate policy in its April meeting by raising slightly the slope of its policy band, while keeping the width and level at which it is centered unchanged. This makes it the first Asia-ex-Japan central bank to tighten policy post Iran conflict, outside of Australia in the broader Asia Pacific region. In its policy statement, MAS raised its inflation forecasts to 1.5-2.5% from 1-2% previously for both headline and MAS core inflation, while lowered its assessment of growth. In particular, MAS said that that GDP growth in 2026 as a whole is likely to step down from the above trend pace recorded in 2025, and that concomitantly the positive output gap will narrow to around zero percent. This is a downgrade from the previous assessment in the January statement of a positive output gap for 2026. Overall, the MAS highlighted the highly uncertain impact of the Middle East conflict on both growth and inflation, even as its assessment is that energy supply shocks are likely to remain persistent in different scenarios and as such continue to push up input costs in the months and quarters ahead.

In the immediate aftermath of the policy meeting, we saw a knee-jerk reaction higher in USD/SGD, with S$NEER also moving as such, to around 0.5-0.6% below the upper bound of the exchange rate band by our estimates. This may partly reflect the pricing and expectations of markets currently for tightening, as proxied by FX forward markets. With the current slope of S$NEER policy around 1% in April 2026 from 0.5% previously, FX forwards already seem to imply and price for S$NEER griding higher at current settings over the next 12 months. The next move as such is likely to depend on any upside or downside surprises to MAS’ inflation and output gap assessments.