Ahead Today

G3: Japan tertiary industry index

Asia: China loan prime rates, Malaysia trade, Philippines BOP

Market Highlights

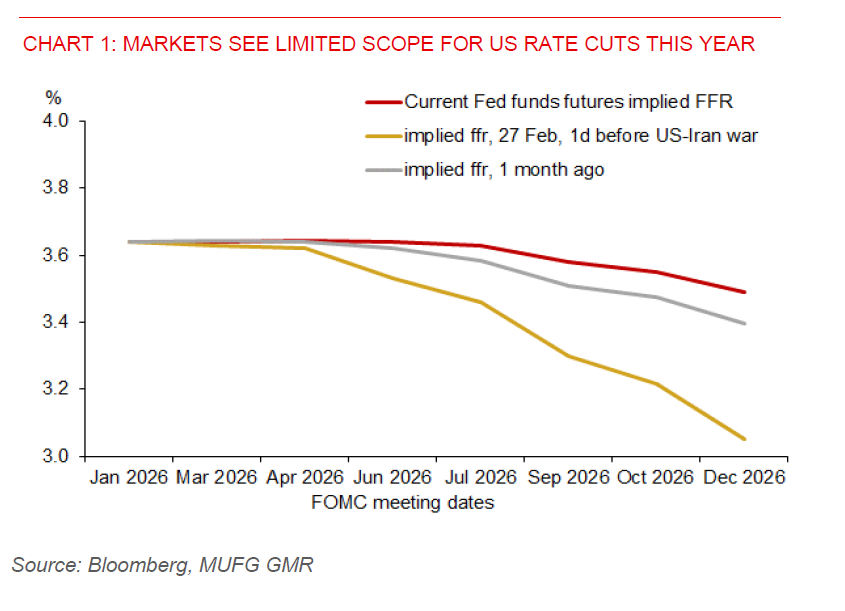

The S&P 500 index has recovered to pre‑war levels, while Brent and the USD have softened. However, market sentiment is likely to remain fragile. Without tangible progress in US–Iran diplomacy or an extension of the current two-week ceasefire, the gap between optimistic pricing and realities on the ground - closed Hormuz routes, tighter energy supply, and structurally higher energy demand - argues for caution. Rates markets echo this tension, with markets pricing out US rate cuts this year, suggesting easing expectations remain constrained by inflation and geopolitical risks.

Markets remain sensitive to Middle East developments, with focus on whether de‑escalation signals are credible or merely episodic noise driving volatility. While there is speculation around renewed high‑level US–Iran engagement, no formal talks are scheduled yet, Iran has reportedly rejected negotiations, and the Strait of Hormuz remains closed. This keeps the backdrop fundamentally tense, especially as the US naval blockade aimed at restricting Iranian oil exports has already seen multiple vessels turned away, underscoring real and ongoing supply disruption. The US Navy has also reportedly seized an Iranian cargo ship in the Gulf of Oman.

That said, several Asian currencies are drawing support from a resilient CNY and the regional tech upcycle, helping to cushion FX against global risk volatility. China’s Q1 GDP grew 5.0%yoy, beating market expectations and keeping growth at the upper end of official targets. This stronger backdrop has kept CNY trading firmer than pre‑US–Iran conflict levels, reinforced by consistently lower daily USDCNY fixings, and will act as an anchor for regional sentiment. MYR stands out as a potential beneficiary given its close correlation with CNY. Malaysia’s economy also held up well in Q1, expanding 5.3%yoy, easing from 6.3%yoy in Q4 2025 but still reflecting healthy momentum. Growth was broad‑based, led by manufacturing (+5.8%) and services (+5.4%), in line with strong investment approval trends across both sectors.

The regional tech upcycle remains a key anchor too: Taiwan’s exports surged 61.8%yoy in March on semiconductor strength, while Singapore’s electronics exports jumped 74%yoy. Upcoming Malaysia trade data may also point to sustained strength in its electrical and electronics exports, reinforcing the view that the regional tech cycle remains intact and is supportive for tech‑linked Asian FX.