Ahead Today

G3: US ADP employment, retail sales, pending home sales; Germany ZEW survey

Asia: Taiwan export orders

Market Highlights

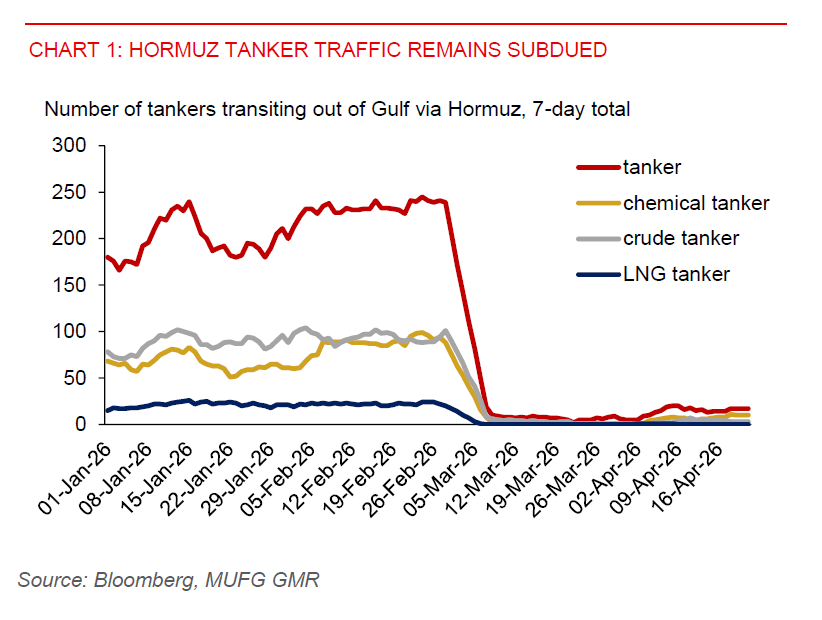

Markets are currently priced for de-escalation. But any escalation, particularly military action around Hormuz, could trigger a renewed spike in oil prices and a broad risk off move. The two-week US–Iran ceasefire expires on Wednesday. The key question for markets is whether President Trump delivers another “TACO” outcome - extending the ceasefire or de-escalating tensions - or instead up the ante. President Trump has signalled he is unlikely to extend the ceasefire, while the US blockade of the Straits of Hormuz, aimed at restricting Iranian oil exports, could remain unless a deal with Iran is reached. With conflicting signals on whether Iran will engage in further peace talks and no formal timeline set, outcomes remain binary. Hormuz tanker traffic also remains subdued.

Separately, President Trump’s Fed Chair nominee Kevin Warsh testifies before the Senate Banking Committee today. Against the backdrop of higher gasoline prices and sticky inflation risks, Warsh is likely to strike a cautious tone, balancing calls for rate cuts with the need to preserve Fed credibility. While unlikely to sound overtly dovish, we expect him to keep the door open to lower rates over time

Several regional currencies have remained relatively resilient, despite the ongoing energy shock. This resilience leaves them vulnerable to negative surprises, particularly a renewed spike in oil prices should the US escalate militarily to seize control of the Straits of Hormuz. Such a scenario would have implications for global inflation and Asia’s growth outlook, posing downside risks for regional FX.

That said, the regional tech upcycle remains a near term bright spot. Malaysia’s exports rose 8.3%yoy in March, easing from 10.7% in February, with electronics exports still robust at +15.0%yoy and +26.7% year to date. While this performance lags the outsized gains seen in Singapore’s electronics exports (+74%yoy) and Taiwan’s total exports (+61.8%yoy), it nonetheless reinforces the resilience of the broader Asian tech cycle. The ringgit, however, remains largely unresponsive to the data, with markets likely staying focused on Middle East risks.

In contrast, the Indonesian rupiah has been an Asia underperformer, reflecting lingering concerns over the impact of higher energy prices on Indonesia’s fiscal position. That said, IDR appears cheap from a valuation standpoint, and from a flow perspective, foreign participation in the local bond market is showing tentative signs of stabilization. While net inflows remain modest, they mark a clear improvement from the sharp outflows seen in March and are consistent with the recent moderation in 10-year Indonesian yields to around 6.5-6.6% after peaking near 7%.