Ahead Today

G3: Speech by Fed’s Daly

Asia: Malaysia Q1 GDP and CPI, Thailand international reserves

Market Highlights

Markets have broadly taken comfort from tentative diplomatic progress in the Middle East, even as a decisive resolution remains uncertain. With US–Iran diplomacy potentially heading into a second round this weekend, and Israel–Lebanon agreeing to a 10-day ceasefire, geopolitical risk premia are being unwound in US equities. Interestingly, the S&P 500 index has rebounded above pre-war levels and volatility has eased sharply.

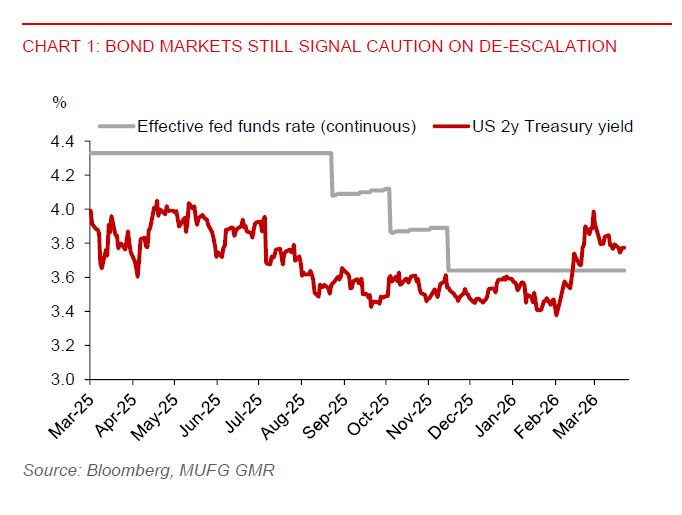

FX-wise, the USD has also softened on improved risk appetite, but still-high US front end rates are keeping a supportive carry backdrop for the dollar, with the US 2-year yield remaining above the effective Fed funds rate (albeit easing). It appears that bond markets are still signalling some caution about the de-escalation narrative.

Meanwhile, Asian FX has also rebounded as markets price for a quicker resolution. If there is indeed a quick or credible path to resolution, recent optimism could persist, feeding into our medium-term view of eventual dollar weakness. However, if diplomacy fails and optimism fades, USD could stay supported for longer, while recent Asian FX gains look more vulnerable, amid still high energy prices.

In Asia, a firmer CNY has provided a key anchor for regional sentiment. This anchor is reinforced by a solid start to China’s economy in Q1, offering timely support at a challenging juncture. China’s GDP grew 5.0%yoy in Q1, at the upper end of the government’s 4.5%–5.0% growth target for the year, driven by resilient exports and strong production in new growth sectors. Output in high tech industries rose 12.5%, while industrial robot and integrated circuit production jumped 33% and 24% respectively. This strength has helped to cushion some moderation seen in retail sales (+1.7%yoy in March vs. 2.8% average in Jan-Feb).

Encouragingly, China’s strong high-tech output growth corroborates Taiwan’s March export data, which showed a sharp 61.8%yoy rise, driven largely by semiconductors and electronics. This reinforces our view that the regional tech upcycle remains intact. Against this backdrop, tech -oriented currencies such as TWD, KRW, SGD, and MYR should continue to benefit.

A key regional focus today is Malaysia’s Q1 GDP advance estimates and March CPI release. Resilient domestic demand, alongside exports in palm oil and electronics, should continue to underpin the ringgit. While diesel prices have risen, the near-term inflation impact in March is likely cushioned by the government’s decision to maintain the RON95 fuel price subsidy at RM1.99/litre.