Ahead Today

G3: US S&P PMI, Eurozone PMI

Asia: India PMI, Australia Employment

Market Highlights

The dominant macro theme entering Thursday's Asian session is the US-Iran conflict and its sustained disruption to Strait of Hormuz energy flows, which has driven global long-bond yields to their highest levels since the 2008 financial crisis and placed broad pressure on oil-importing Asian currencies. That backdrop shifted materially late in New York trade on Wednesday when President Trump told reporters the US is in the "final stages" of negotiations with Iran — adding that no sanctions relief would be granted until a deal is formally signed, and that failure to reach agreement would prompt swift military action. The comments sent WTI crude down as much as 7%, settling at $98.26/bbl, while Brent settled at $105.10/bbl. US 2- to 10-year Treasury yields fell approximately 10 basis points, the S&P 500 broke a three-day losing streak, and EM currencies jumped. Iran was reportedly still reviewing the text of any proposed agreement and had not yet formally responded as of Wednesday evening, leaving the durability of the rally the central question for today's session.

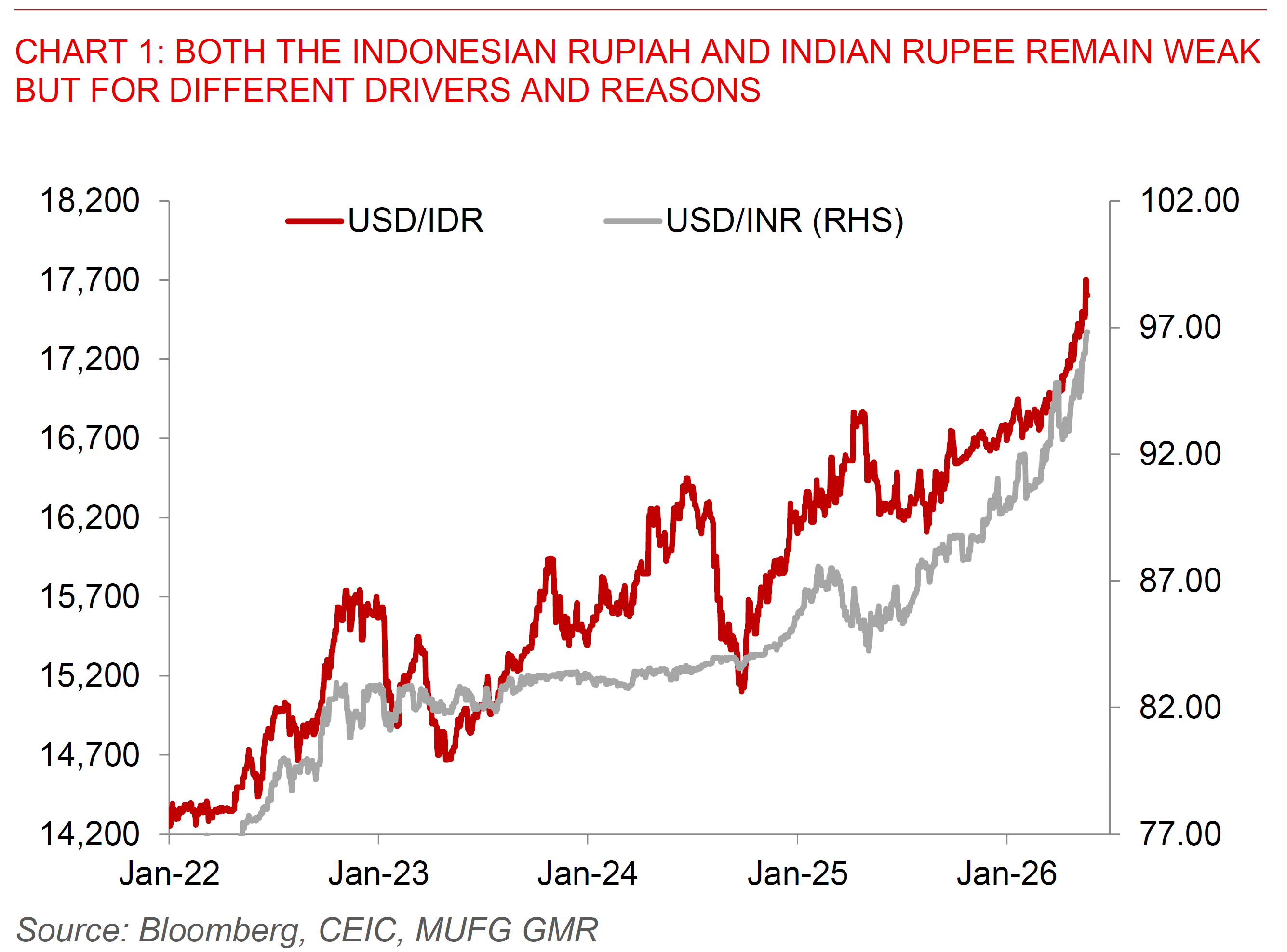

Indonesia was the standout story in Asia on Wednesday, with two major policy developments landing simultaneously. Bank Indonesia raised the BI-Rate by 50 basis points to 5.25% — the first hike since April 2024 and the first 50bp move since November 2022 — surprising the vast majority of market participants, with only one of 41 surveyed economists having forecast a move of that size. Governor Warjiyo framed the decision as a measure to reinforce rupiah stabilisation against heightened global volatility, and stated that the central bank expects the rupiah to strengthen with domestic FX demand likely to ease from July. USD/IDR slipped as much as 0.5% to 17,610 on Wednesday — its biggest single-day gain since early April — while the 10-year Indonesian government bond yield rose 4 basis points to 6.81%. Separately, President Prabowo announced in a parliamentary address that Indonesia will centralise exports of palm oil, thermal coal, and ferroalloys through a single state-owned enterprise — reportedly to be named PT Danantara Sumberdaya Indonesia — supervised by Danantara and set to begin operations as early as June 2026. The policy triggered sharp equity losses: the Jakarta Composite fell 3.5% on Tuesday when rumours first circulated, extending its year-to-date decline to over 26%. The near-term concern for capital flows is that while centralised commodity export receipts could in theory improve FX repatriation over time, the policy has raised immediate questions around governance and investor predictability.

Elsewhere across Asia, the Indian rupee touched a record low of 96.9650 on Wednesday before the RBI intervened by selling dollars in the onshore market, pulling USD/INR back to around 96.83. India's 364-day T-bill yield surged 21 basis points to 5.975% at auction — the largest move in nearly four years — signalling that markets are beginning to price potential RBI rate action. In Japan, Wednesday's 20-year JGB auction provided short-term relief, drawing a bid-to-cover ratio of 4.01 against a 12-month average of 3.43, at an average yield of 3.711% — the highest since 1996 — with the 20-year yield subsequently falling as much as 10 basis points. Markets are pricing approximately an 80% probability of a 25bp BOJ hike at the June 15–16 meeting, and Japan's Finance Minister delivered strongly worded verbal intervention on Wednesday to support the yen. The key watch points for today are any formal Iranian response to the US proposal, further operational details on Indonesia's new commodity export entity, and Australian employment data due this morning.