Ahead Today

G3: US Non-Farm Payrolls

Asia: Singapore PMI

Market Highlights

Overall the US Dollar was stronger with the combination of lower than expected CPI in Europe, mixed comments from Kevin Warsh, and ahead of non-farm payrolls numbers out later today. In particular, Eurozone CPI came in at 2.8%yoy, down from 3.2%yoy, and was below the consensus expectations of 3%yoy. Core inflation in Europe also came in softer at 2.4%yoy. On that back of this, we saw ECB Governing Council member Yannis Stournaras saying that he sees a smaller likelihood of further rate hike with the fall in energy prices and slowing eurozone inflation, and that it is perhaps good to stay where the ECB is right now.

For the Fed, we saw a range of comments from Warsh in the Sintra Forum which partly reiterated what was mentioned during his first FOMC meeting, with a commitment to achieving price stability coupled with a desire to change the Fed’s communication strategy to focus less on forward guidance and spoon-feed the market less. Nonetheless, he also mentioned that the Fed should not fear strong productivity-led growth, and that it would be a mistake to raise rates during an AI-led productivity boom because that boom would allow the supply of goods and services to catch up with demand and keeping inflation in check even with a stronger economy.

Overall, while it will take time for Warsh’s views to be digested more completely by markets, it seems quite likely that he will deliver changes at the Fed – and potentially big and important ones. So far he has been extremely impressive in his communication and his messages, and with that answering the questions he wants to and sidestepping the questions that he doesn’t. From a markets perspective, our bias is to think that rates will become more volatile moving forward and that the yield curve may become steeper, or at the very least the back-end of the US curve may not have space to fall much given his desire to reduce the size of the Fed’s balance sheet over time. FX may as such also follow through with greater US rates volatility, with the bias towards the Dollar being supported in the very near-term until we get better clarity on the macro data and dynamics in the US.

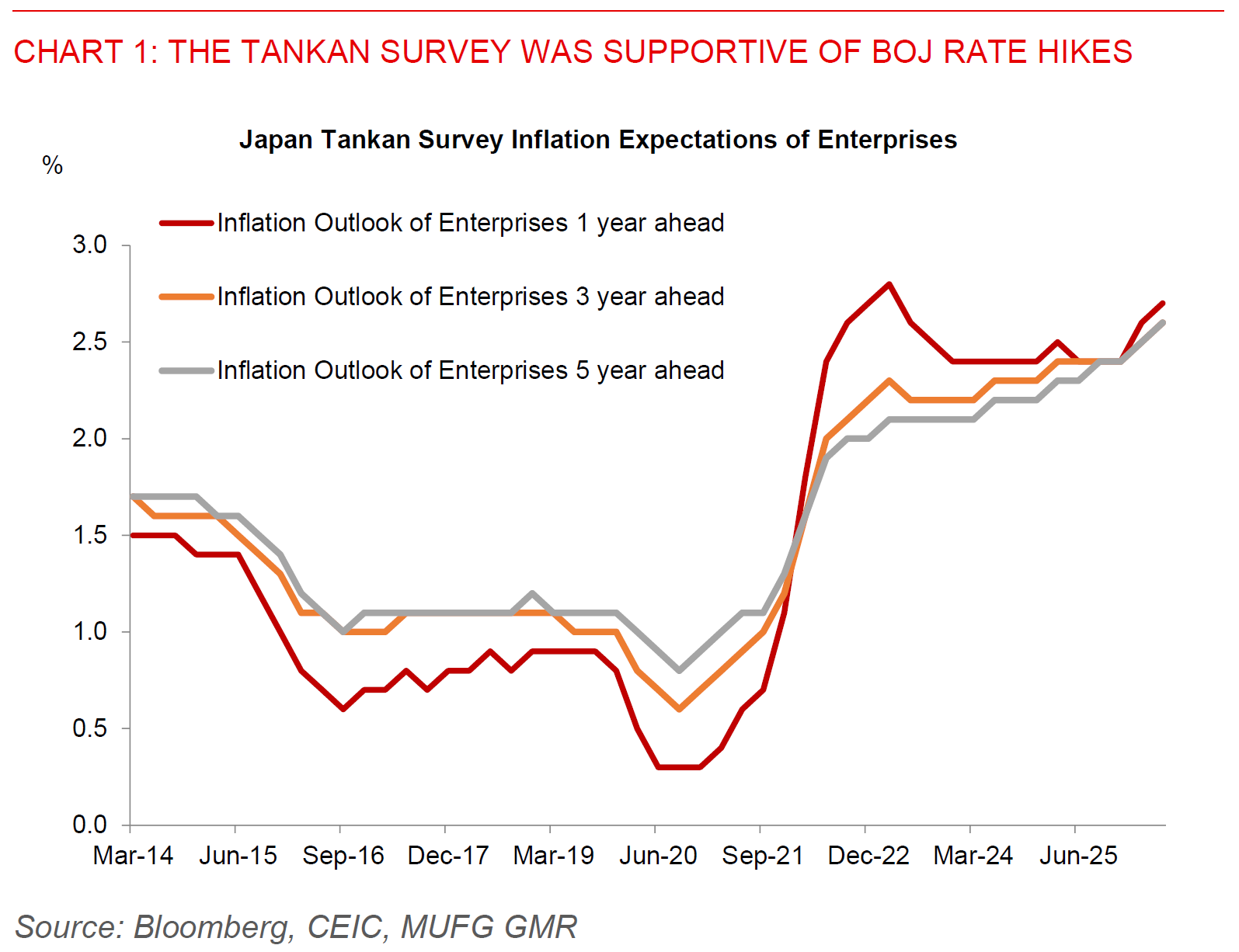

The one place where rates clearly have to head higher is in Japan. Yesterday’s Tankan survey was overall positive even as the survey responses were provided before the announcement of the US-Iran agreement. For one, appetite for capital investment by large enterprises remains strong. Second, the outlook for selling prices and inflation expectations rose further. While we think the BOJ should be raising rates and likely sooner rather than later, a key question by markets is to what extent the government will push back against that, and with that the release valve in the near-term will likely have to be a weaker exchange rate in higher USD/JPY.

We would be quite wary in the near-term though of intervention risks, given the bias for Japanese authorities to intervene during periods of low liquidity and also if US data is supportive of the directional bias for Japan’s Ministry of Finance. With the upcoming NFP numbers, coupled with key US holidays next week, we could have a risk of intervention over the coming week.