Ahead Today

G3: US mortgage applications

Asia: BI policy rate decision, Malaysia foreign reserves

Market Highlights

A second round of US–Iran talks failed to materialize after Tehran rejected further peace discussions, following an initial high level engagement that did not yield any resolution to the conflict. President Trump has unilaterally extended his ceasefire timeline, keeping a temporary truce in place until talks with Iran are formally concluded. The initial two-week truce is expected to expire later today. Meanwhile, the US continues to blockade Iranian ports to halt oil shipments. The conflict appears to have moved into a prolonged standoff rather than towards a swift or durable resolution, with US leveraging the port blockade to pressure Tehran into a peace deal, or risk further military escalation.

For markets, this environment implies continued disruption to energy flows through the Strait of Hormuz. Brent crude for June delivery remains elevated, hovering near the USD100/bbl level. However, broader macro markets remain relatively contained, with DXY steady around 98.4 and the US 10-year Treasury yield holding near 4.3%.

On the macro data front, US ADP employment increased by 54.75k in the week ending 4 April, up from 40.25k previously. Retail sales excluding autos and gasoline also rose a firm 0.6%mom in March, matching the pace seen in February, pointing to continued resilience in US consumer demand.

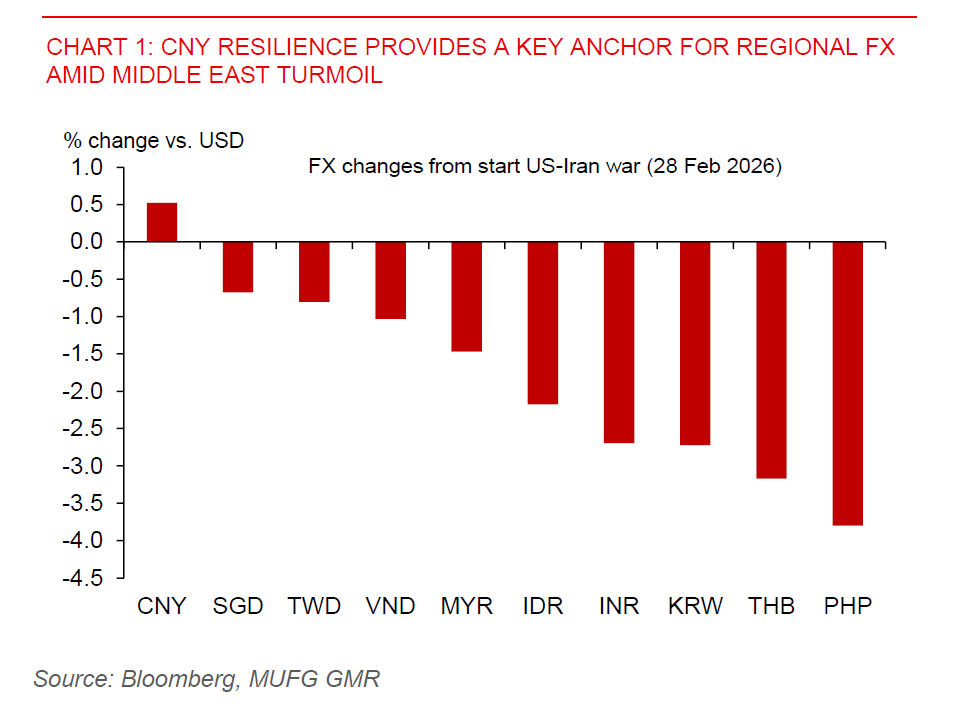

Despite ongoing Middle East turmoil, Asian FX has shown relative resilience. CNY, in particular, has strengthened by around 0.5% against the USD since the conflict began, underpinned by solid exports and continued PBOC support. SGD has also held up well, supported by MAS’s policy tightening and Singapore’s substantial macro and policy buffers. TWD continues to benefit from the global tech upcycle, a theme that should also lend some support to KRW and MYR at the margin.

However, stress points remain more visible in high oil sensitivity currencies. PHP is vulnerable given its heavy reliance on Middle Eastern crude imports, while THB runs the largest oil and gas trade deficit in the region. That said, the overall decline in Asia FX has so far been relatively modest compared to the sharp dislocations seen during the Russia–Ukraine conflict.

A key regional focus today is Bank Indonesia’s policy rate decision. BI continues to prioritise rupiah stability and is expected to keep policy rates unchanged. We see BI on hold through Q2, with rate cuts only becoming viable once the rupiah has clearly stabilised. Our base case remains for near term USDIDR stabilisation rather than a disorderly depreciation. We maintain our end Q2 USDIDR forecast at 17,000 and look for gradual improvement in rupiah performance in subsequent quarters as stabilisation forces build.

Active FX intervention has helped contain volatility and slow the pace of USDIDR upside, while Indonesia’s sovereign CDS spreads have narrowed. An underappreciated upside support for the rupiah is the positive spillover from higher energy prices into non energy commodity prices, which should provide a partial offset to external pressures.