Ahead Today

G3: US Fed FOMC Meeting

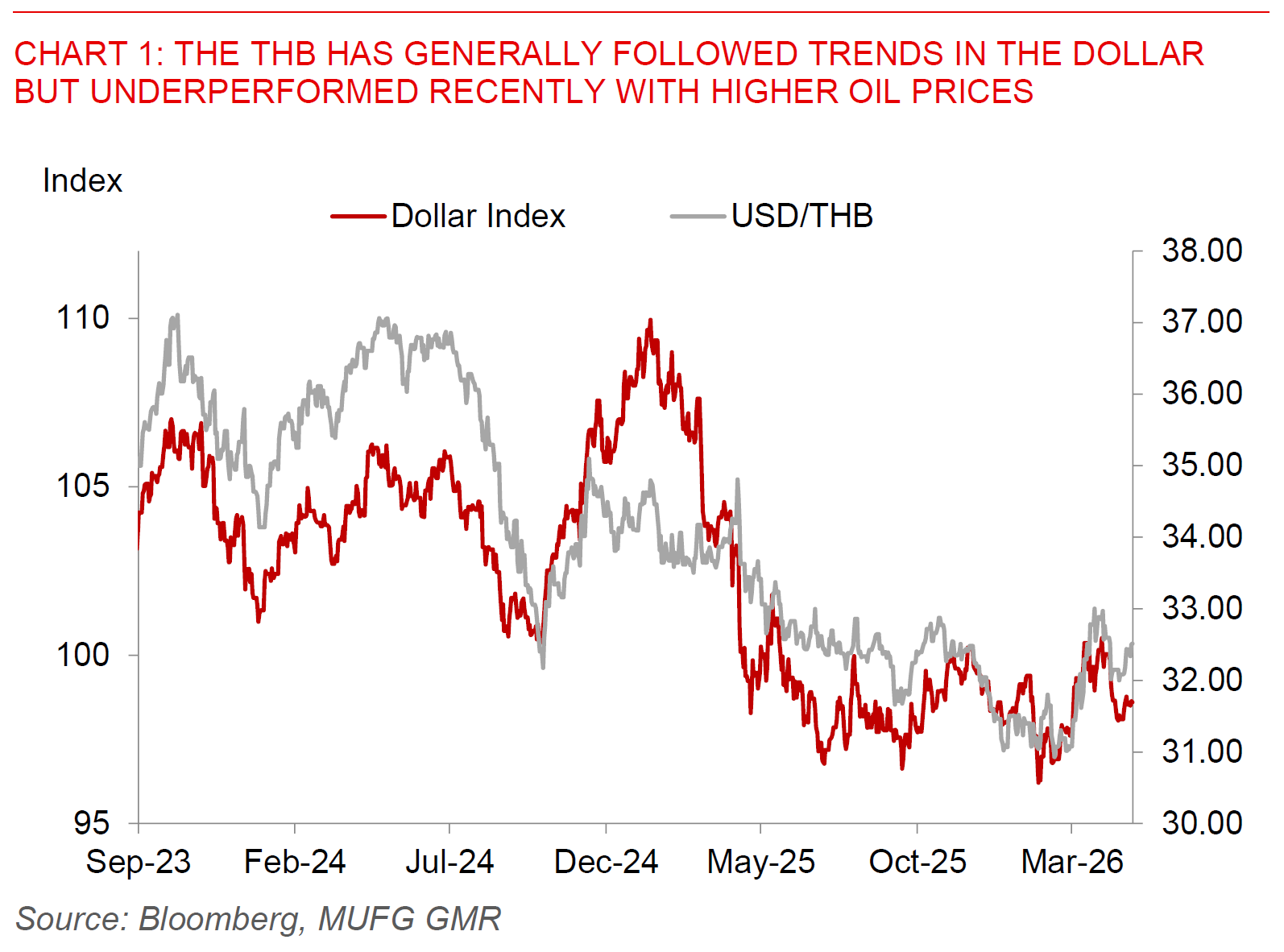

Asia: Bank of Thailand policy decision

Market Highlights

President Trump said Iran has asked US to lift a naval blockade of the Strait of Hormuz while the two sides negotiate an end to the two-month war. According to Trump, Iran wants the Strait open “as soon as possible”, while according to Trump said that Iran is in a “State of Collapse” as “they try to figure out their leadership situation”. On Iran in particular, while nobody quite knows completely what is happening within, the fact that its decisions overall have collectively been strategically sound, and certainly much more so than what we have seen so from the US so far tells us that there is some institutionalized collective decision making in the country. Of course the system is now more hardline, less amenable to concessions, and believes that it now has far more leverage through the Strait of Hormuz to ensure its survivability. But the important point is that Iran’s steps have thus far been rational and as such any notion that Iran is in a “State of Collapse” is to our minds more bluster. Overall, we think in forecasting the path forward on the Middle East conflict it’s more important to see what Trump does rather than what he says. To our minds, the bar for further military escalation seems quite high at this point in time, and Trump will no doubt want to try his best to seek a deal. Whether he can ultimately do so is of course another matter.

Beyond the Iran conflict, UAE announced in a surprise decision yesterday that it is quitting OPEC/OPEC+ starting 1 May. While this has been talked about internally within UAE for some time, the timing with the ongoing war and perhaps also the manner in which it was done was probably the more important surprise. Overall, the drivers among others seems to be dissatisfaction within UAE on production quotas by OPEC, and with Abu Dhabi having built up significant investment and spare capacity already this means that in theory oil production could be ramped up over time from around 3mb/day to perhaps up to 5mb/day after the crisis ends. Other key drivers of UAE’s decision could include disagreements with Saudi Arabia more broadly on a range of issues. The key question is also whether other members of OPEC/OPEC+ may see fit to leave the group, and ultimately erode the effectiveness of the group. Putting it all together, the near-term implications are minimal, but longer-term this could remove the effectiveness of OPEC to put a floor on oil prices and as such bias oil prices to be lower rather than higher over time.

We will have the FOMC and Fed meet, which will be the swan song and last meeting for Jerome Powell as Chair of the FOMC. Overall, our base case is for a neutral statement in Powell’s last FOMC chaired event, and for Powell to continue to say they need more data to assess the full impact of disruptions to energy and energy related prices (see FOMC preview April 2026).

The Bank of Thailand’s policy meeting today will likely see the BOT keep rates on hold at 1%, and as also guided previously by BOT Governor Vitai Ratanakorn. The BOT will likely want to look through the inflation shock as much as possible, and with that fiscal policy including through cash handouts and subsidies through domestic fuel and diesel prices should take more of a role in managing the shock from the Middle East Conflict. Overall, this also means that the BOT will unlikely push back too much against currency weakness, and this will leave USD/THB ultimately dependent on how the SoH crisis plays out moving forward.