Ahead Today

G3: US Consumer Confidence, US Dallas Fed Manufacturing Activity

Asia: Singapore Industrial Production

Market Highlights

Markets continued to show some optimism surrounding a US-Iran deal amidst negotiations, even as there was some renewed fighting in the Persian Gulf and unclear signals from Israel around the commitment to ceasefire in Lebanon. In particular, Trump said that negotiations with Iran over an interim deal to extend the ceasefire and reopen the Strait of Hormuz were “proceeding nicely”, with an Iranian delegation travelling to Doha for consultations with senior Qatari officials on the negotiations. The us and Iran still need to finalise key details, including whether ships transiting the Strait of Hormuz will be allowed free passage, and how quickly billions of dollars of Iranian funds will be unfrozen. Overall, markets rallied and on the FX side we saw the Dollar weaken and Asia currencies generally trading stronger on the back of these developments.

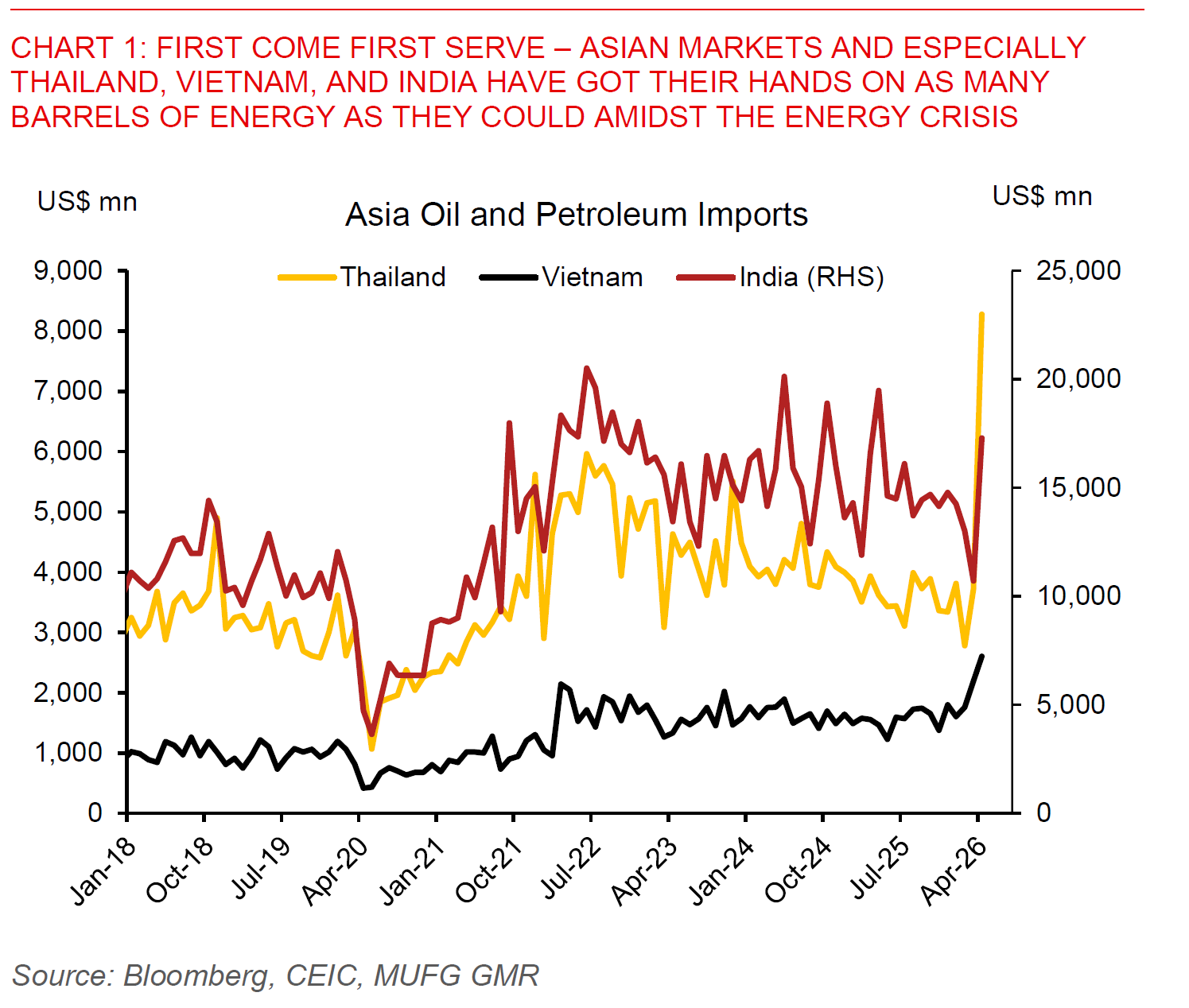

Moving forward, even if the Strait of Hormuz were to re-open today, it will take some time for the physical barrels of oil and energy to flow through. For Asian markets, what has helped – or also affected markets – has been a sharp rise in precautionary energy demand, which we have seen in the trade reporters for April so far. The likes of Thailand, Vietnam, and India in particular saw sharp jumps in crude oil imports, as all 3 countries got their hands on as many barrels as they possibly could especially outside the US. In many cases, the data show that petroleum imports from the likes of Russia, Brazil, the US and to some extent Angola has picked up, and showcasing the lengths to which Asian countries have gone to secure energy for their citizens – at some cost of course.

For Asia FX and rates markets, we think there are at least three key risks which will have to be monitored closely, and will be a potential source of differentiation in asset prices moving forward. First the risk of a “Super El-Nino” event and how that will interact with both the earlier spikes in energy prices and as such ultimately food prices and inflation. Second, the risk of possible Fed rate hikes and higher US yields, even as we stress that this is not our base case. And third, the risk of rising domestic policy uncertainty and with that leading to greater capital outflows and/or dearth of inflows, and with weaker FX a key constraint moving forward from a policy perspective. Certainly in Asia, India, Indonesia, and the Philippines could be more vulnerable when you look at the totality of all three risks combined, and it’s interesting as well that the Indonesian Rupiah failed to rally and actually weakened yesterday despite the good news that we have seen on the US-Iran negotiations.