Ahead Today

G3: US JOLTS Job Opening

Asia: Philippines trade, China PMI, Thailand Current Account

Market Highlights

The US Supreme Court voted 5-4 that Fed Governor Lisa Cook can stay in her job while she fights Trump’s bid to oust her over unproven mortgage fraud allegations, providing some tentative support for Fed independence against Trump’s pressure to cut interest rates for the time being. The Supreme court justices ultimately faulted President Trump for not giving Cook notice and a chance to be heard before trying to remove her from her position, but stopped short of saying whether the allegations against Cook would be sufficient grounds for removing her. In a separate case, the Supreme Court expanded Trump’s executive power by allowing him to fire a Federal Trade Commission member, reiterating previous suggestions that the Fed is different from other federal agencies because of its role in setting monetary policy.

Overall, given that the ruling continues to open the possibility of Trump trying again to remove a Fed official due process notwithstanding, this continues to raise concerns about the sustainability of Fed independence moving forward. From an FX perspective, while the Dollar has been supported thus far by the Fed turning more hawkish and Kevin Warsh in his first FOMC meeting supportive of the focus on price stability, questions around Fed moving forward may at the very least cap upside in the Dollar.

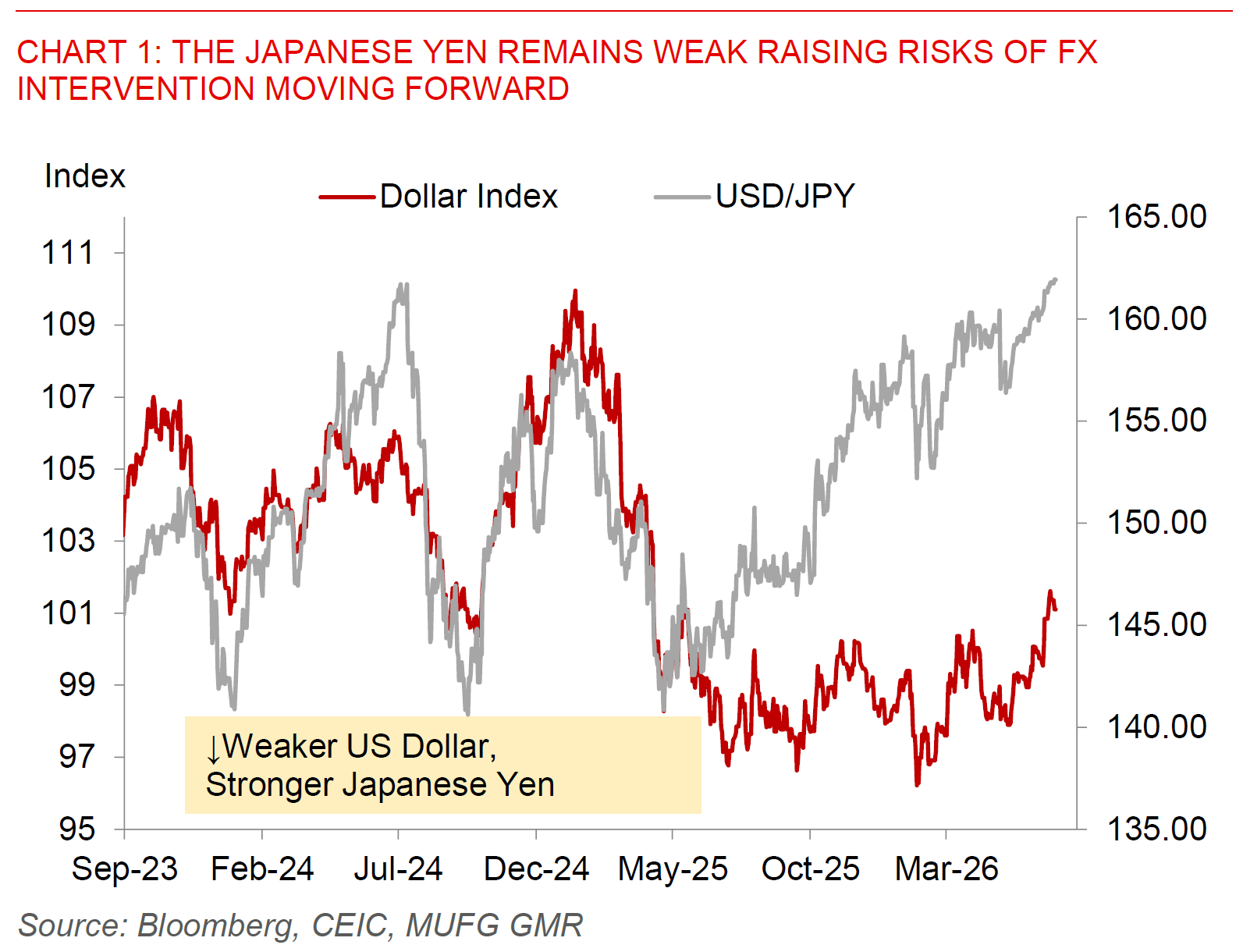

Overall, while we saw the Dollar weaken somewhat on these developments, USD/JPY in the near-term moved against these trends closer to the key level of 162, raising continued prospects of intervention moving forward. Markets are concerned about the extent of possible government pushback against Bank of Japan rate hikes, with Bloomberg News reporting that the draft of PM Takaichi’s basic policy guidelines is expected to show BOJ working closely with the government to confirm a positive cycle of wages and prices and sustainability reach the 2% price stability target. For USD/JPY to durably change trend moving forward, we would need BOJ to turn more hawkish to lift negative real interest rates further.

The other key focus of markets in our region was the implicit rate setting of PBOC’s new overnight liquidity tool. This came in at 1.25% according to news reports, although the coupon rate was not explicitly announced by the central bank, with PBOC only saying that it conducted 300 billion yuan (US$44bn) of overnight reverse repurchase agreements in OMOs yesterday. While this follow PBOC Governor Pan Gongsheng’s remarks at the recent Lujiazui Forum on further refining China’s interest rate framework, we still think the 7-day reverse repo rate remains the primary tool for now with the overnight rate serving as a supplementary liquidity fine-tuning instrument. Over the medium-term, the PBOC will likely shift towards the overnight rate as the policy anchor but this will take some time.