Ahead Today

G3: US initial jobless claims and PPI

Asia: Thailand consumer confidence

Market Highlights

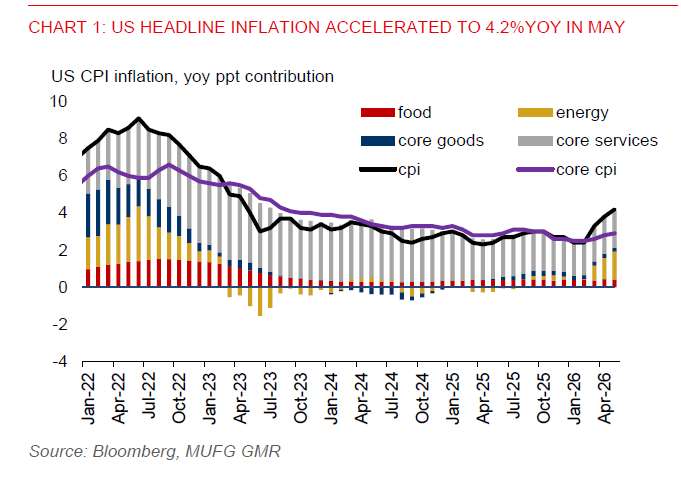

US CPI accelerated to 4.2%yoy in May (from 3.8%), with core inflation rising modestly to 2.9%yoy, broadly in line with expectations. The upside in headline inflation was largely driven by energy, reflecting the ongoing geopolitical shock from the US–Iran conflict. Energy contributed 1.5pp to headline inflation in May (up from 1.1pp in April) and accounted for nearly 60% of the monthly increase. While US retail gasoline prices have eased in recent weeks, they remain elevated relative to pre-conflict levels, continuing to feed through into inflation and keeping inflation expectations sticky. In this context, the University of Michigan’s 1-year inflation expectations rising to 4.8% underscores a growing risk of second-round inflation effects, which in turn limits the Fed’s scope to ease policy. This reinforces the “higher-for-longer” rates narrative and supports the USD via firmer front-end yields.

At the same time, geopolitical risks have re-escalated, with renewed military strikes between the US and Iran alongside stalled diplomatic negotiations. Importantly, traffic flows through the Strait of Hormuz remain subdued, keeping the energy supply outlook uncertain. The balance of risks has therefore shifted in a more asymmetric direction for Asian currencies, with downside risks dominating. If tensions persist into Q3, elevated oil prices and weaker global risk sentiment are likely to remain a headwind for Asia FX. Market pricing also reflects declining confidence in a near-term US–Iran resolution, suggesting geopolitical risk premia are likely to remain embedded over the near term.

The transmission into Asia’s macro fundamentals is becoming increasingly evident. Higher oil prices are driving a deterioration in terms of trade for net oil importers, while trade balances are weakening, most visibly in economies such as Thailand, the Philippines, and Indonesia. Historically, higher oil prices have been associated with a material worsening in current account balances and inflation dynamics across Asia, reinforcing depreciation pressures on FX.

In FX markets, this backdrop has supported upside momentum in several USD/Asia pairs. The Thai baht stands out as particularly vulnerable to prolonged Middle East conflict. Thailand runs one of the largest net oil and gas trade deficits in the region, leaving its external position highly exposed to energy price shocks. At the same time, domestic yields remain relatively low, while headline inflation has rebounded towards 3% in May following a period of deflation in 2025, eroding the baht’s real carry attractiveness. This combination of weaker terms of trade and limited carry support leaves THB especially exposed to further downside pressure, particularly if Middle East tensions escalate further.