Ahead Today

G3: US University of Michigan sentiment, Germany IFO business climate

Asia: Thailand trade data

Market Highlights

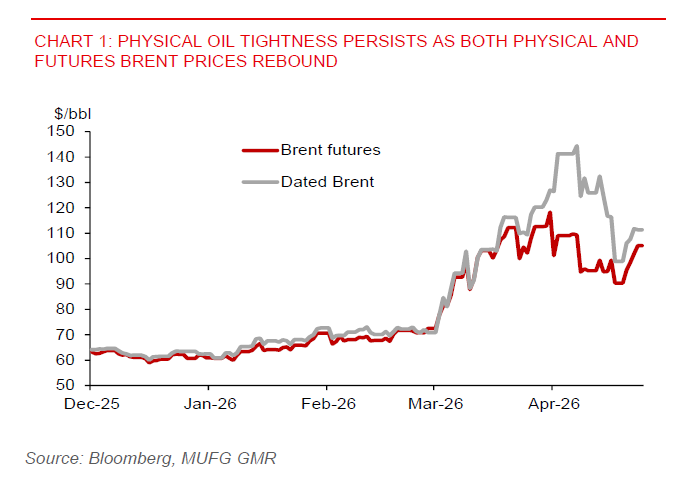

The US dollar has further strengthened toward the 99.00 level, amid higher yields and haven demand. US 2-year yield has inched higher by about 3.6bps to 3.83%, while the US 10-year yield was 4.32%. Energy prices remain a key macro driver. Brent closed higher at around $105/bbl, marking the third straight day of gains and retracing some of the 28% drop from the $119/bbl peak seen on 31 March.

Geopolitics continues to dominate market sentiment. President Trump has said that he was “in no rush” to end the war and has ordered attacks on Iranian ships that are placing mines in the Strait of Hormuz. Reports that Iran is deploying more mines in Hormuz have raised some tail risks. While the Israel–Lebanon ceasefire has been extended by three weeks, Iran appears to be rejecting further peace talks with the US for now, limiting relief for risk sentiment.

On the macro front, US data has leaned supportive of USD strength. Initial jobless claims were at 214k, remaining at low levels. Meanwhile, S&P Global PMI data surprised to the upside, pointing to firmer expansion in both US manufacturing and services activity.

In Asia, THB (-0.8%), PHP (-0.6%) and IDR (-0.7%) led losses versus the US dollar, amid the oil shock impact on their fiscal accounts. USDTHB has rebounded to around 32.40 after finding support at 31.90 level, and looking to re-test the 32.50-33.00 level. The Thai government plans to cut spending to free up THB95b-125b funds to support energy subsidies while keeping the budget deficit targets for this and next fiscal year intact.

While the BSP raised its policy rate by 25bps to 4.5% and signalled for further rate hikes to counter inflation, this won’t provide much support for the PHP, amid the Middle East conflict, oil price shock, and markets expecting Fed to keep rates high for longer. These factors need to turn for PHP to regain strength.

USDIDR has reached fresh all-time highs around 17,300 level. This overshoots our prior near-term stabilisation view around 17,000. This move appears less about global USD strength and more about a domestic confidence shock, with markets likely reacting to heightened fiscal uncertainty. In the near term, upside risks to USDIDR have clearly widened, with sentiment still fragile. The speed and direction of the latest move suggest markets are demanding a higher risk premium, particularly as oil prices remain elevated and fiscal-energy dynamics stay unfavourable. However, at the same time, valuation signals are becoming increasingly compelling, pointing to meaningful rupiah undervaluation versus the US dollar, while technical indicators show USDIDR moving into overbought territory. Policy response functions could become more binding, with Bank Indonesia firmly focused on rupiah stability. Indonesia’s sovereign CDS spreads have not shown the kind of blowout typically associated with a loss of macro anchor.