Market Highlights

The dominant macro theme is a sharp, broad-based global bond selloff driven by war-related inflation pressures stemming from the effective closure of the Strait of Hormuz. US 30-year Treasury yields touched 5.16% during Monday's Asian session — the highest since 2023 — with bond traders increasingly pricing in a potential new era of structurally elevated borrowing costs. Japan's Q1 GDP, released this morning, beat expectations: real GDP grew 2.1% annualised (0.5% quarter-on-quarter), above the 1.7% consensus, supported by private consumption (+0.3% q/q) and a positive net export contribution (+0.3 percentage points). Critically, the GDP deflator rose 3.4% year-on-year against a 3.1% estimate, reinforcing inflation concerns and adding fresh pressure to JGB yields — which already hit their highest since 1996 on Monday — and strengthening the case for a further Bank of Japan rate hike, with markets pricing roughly a 78% probability of a move to 1.0% in June. China's April data, released Monday, delivered a broad miss: retail sales rose just 0.2% year-on-year — the worst since December 2024 — industrial output grew only 4.1%, the weakest in nearly three years, and fixed-asset investment unexpectedly contracted 1.6% in the first four months of 2026, reversing a 1.7% gain in Q1.

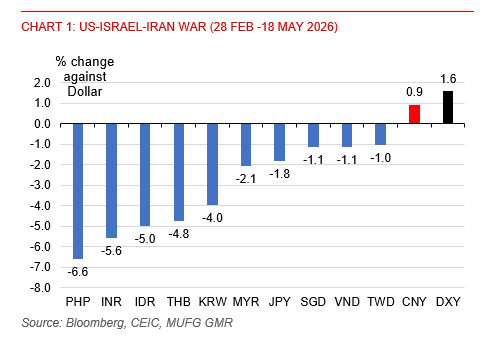

Asia EM currencies are under deepening stress. In Indonesia, the rupiah fell as much as 1.1% on Monday to a record low of 17,663 per dollar — the worst performer in Asia — as markets reopened after a two-day holiday and caught up with the global selloff; the benchmark 10-year bond yield surged 17 basis points, the most in over a year, to 6.86%. The political pressure is intensifying: President Prabowo reportedly summoned economic ministers and the Bank Indonesia governor on Monday as the currency hit its record low. Bank Indonesia has stated it monitors rupiah volatility rather than level, expressed confidence the currency will return to an average of 16,500 per dollar this year, and has raised returns on its SRBI instruments to counter capital outflows — while pledging "smart intervention" across spot, onshore and offshore NDF markets. In India, the rupee closed Monday at a record low of 96.36 per dollar — down 6.7% year-to-date, the worst performance in Asia — while the 10-year government bond yield rose to 7.14%, its highest since May 2024. India's bond market has begun pricing in possible RBI rate hikes later this year, and foreign inflows into Indian bonds have slowed sharply — the 5-day moving average of net buying fell to just $2.1 million against a 20-day average of $47.2 million.

The key variable for today's session is the Iran-US standoff. In a Truth Social post on Monday evening, President Trump announced he was calling off a planned military strike on Iran scheduled for Tuesday, citing requests from the leaders of Qatar, Saudi Arabia, and the UAE, who reportedly told him that "serious negotiations are now taking place" and that a deal — which Trump stipulated must include "NO NUCLEAR WEAPONS for IRAN" — would be reached. Trump added that he has instructed military leaders to remain prepared for a "full, large-scale assault" on a moment's notice if talks fail. The announcement triggered an immediate partial reversal in oil, Treasuries, and EM FX on Monday. However, Iran has stated that any agreement must end the war on all fronts and lift the blockade and sanctions, suggesting the two sides remain far apart. The durability of this de-escalation — and whether it translates into a sustained decline in oil prices — remains the single most important driver for global bond yields and Asia EM currencies in today's session.