Ahead Today

G3: US Mortgage Applications, ADP Employment Change

Asia: Thailand CPI, India PMI

Market Highlights

Brent oil prices fell below US$110/bbl and the Dollar weakened, as President Trump said he would pause a US-led effort to help stranded ships exit the Strait of Hormuz to see if an agreement with Iran to end the war could be finalised. Trump in his social media post said that “Project Freedom” will be paused for a “short period of time” in order to see whether an agreement can be finalized and signed. Nonetheless, Trump said that a US blockade of ships transiting to and from Iranian ports would remain in full force and effect. These developments came on the back of an escalation and initial resumption in hostilities during a four-week ceasefire. Nonetheless there are also some tentative signs that diplomacy and negotiations are continuing, with Iranian Foreign Minister Abbas Araghchi heading to Beijing for talks with Chinese Foreign Minister Wang Yi, and days ahead of Trump’s visit to China to meet President Xi.

Overall, the impact of the Strait of Hormuz as we have been highlighting over the past two months is more than just about oil prices, but also about potential shortages across a whole host of products including energy, petrochemicals and fertilisers. Countries which are more dependent on the Middle East for oil, coupled with those which have less capacity to switch over to a domestic energy production mix and which also depend more on energy and food for imports and consumption are overall more vulnerable to a range of scenarios.

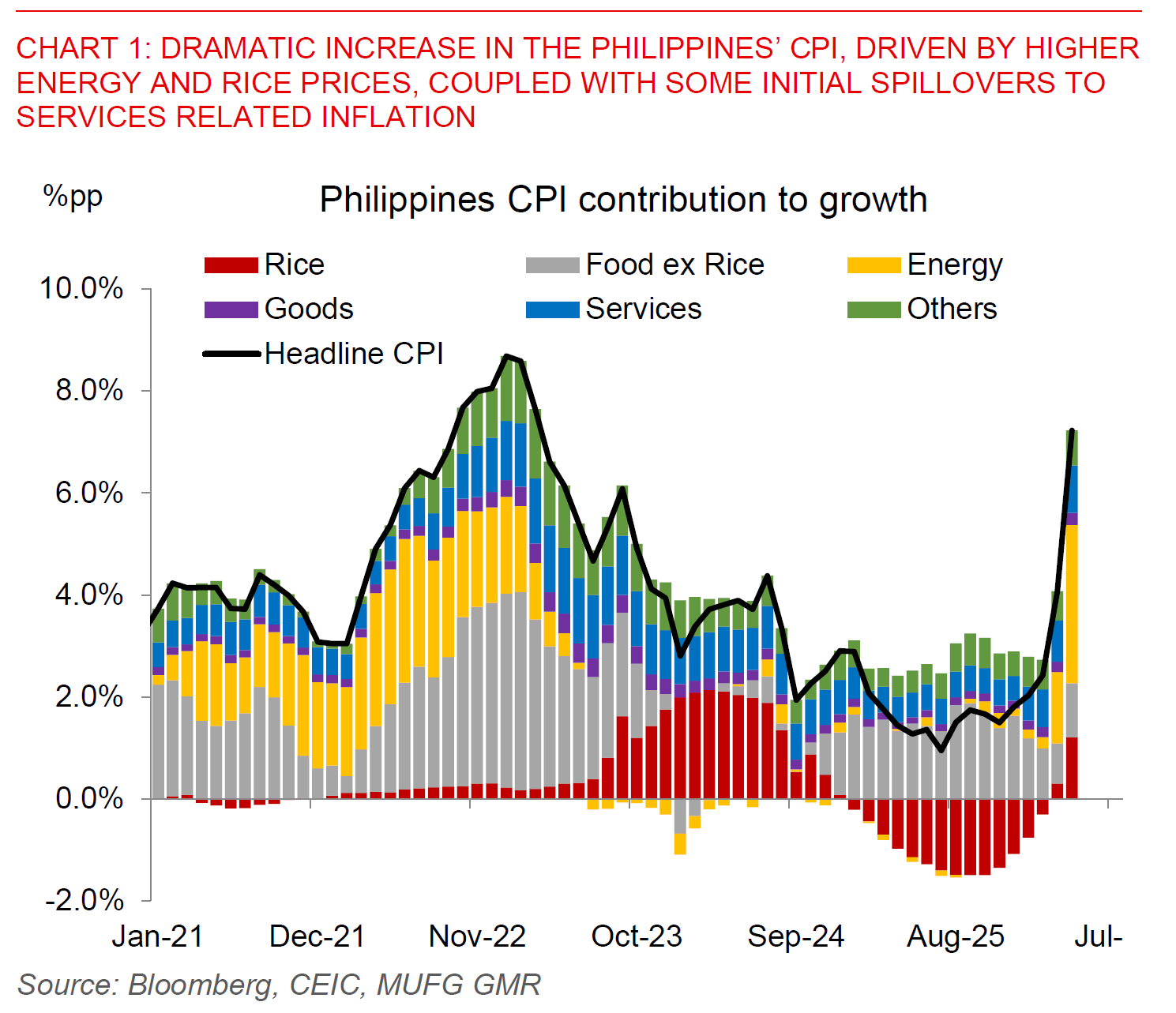

The Philippines as we have been highlighting falls into that vulnerable camp. The data released on the Philippines’ April CPI inflation is indicative and an example of that impact, with headline inflation rising dramatically to 7.2%yoy, well above consensus expectation of 5.5%yoy, and from 4.1%yoy previously. These numbers imply headline CPI rose 2.8%mom sa and core inflation rising by 0.9%mom sa. The details showed that this was driven by sharp increases in energy inflation, including a 24%mom sa rise in transport and a 40%mom spike in gas prices (perhaps reflecting LPG), while food prices such as rice and fish rose further.

Overall, we think BSP will likely have to hike rates further possibly by another 75-100bps this year given the inflation print, and we will not be surprised if there is an off-cycle meeting to do so coupled with perhaps some chance of a jumbo 50bps rate hike moving forward. Nonetheless, given the relatively weak starting point of growth in the Philippines in part driven by the fiscal tightening with the flood control projects scandals, we think that BSP’s focus is more on containing inflation expectations, rather than to target demand destruction given the current negative output gap. Managing the FX passthrough to inflation from a weaker peso is with that also another key objective.

As such, we think there will be a limit to the overall magnitude of BSP rate hikes moving forward, with the central bank certainly caught between a rock and a hard place.

We continue to think that PHP remains vulnerable and should underperform across a range of scenarios, and see USD/PHP possibly rising closer to 62.00 to 63.00 if the Strait of Hormuz remains closed. In our base case of de-escalation, we think USD/PHP could recover gradually towards the 60.50 to 61.50 range.