Ahead Today

G3: US Housing Starts, US Import Price, US Industrial Production

Asia: Malaysia GDP, Malaysia CPI

Market Highlights

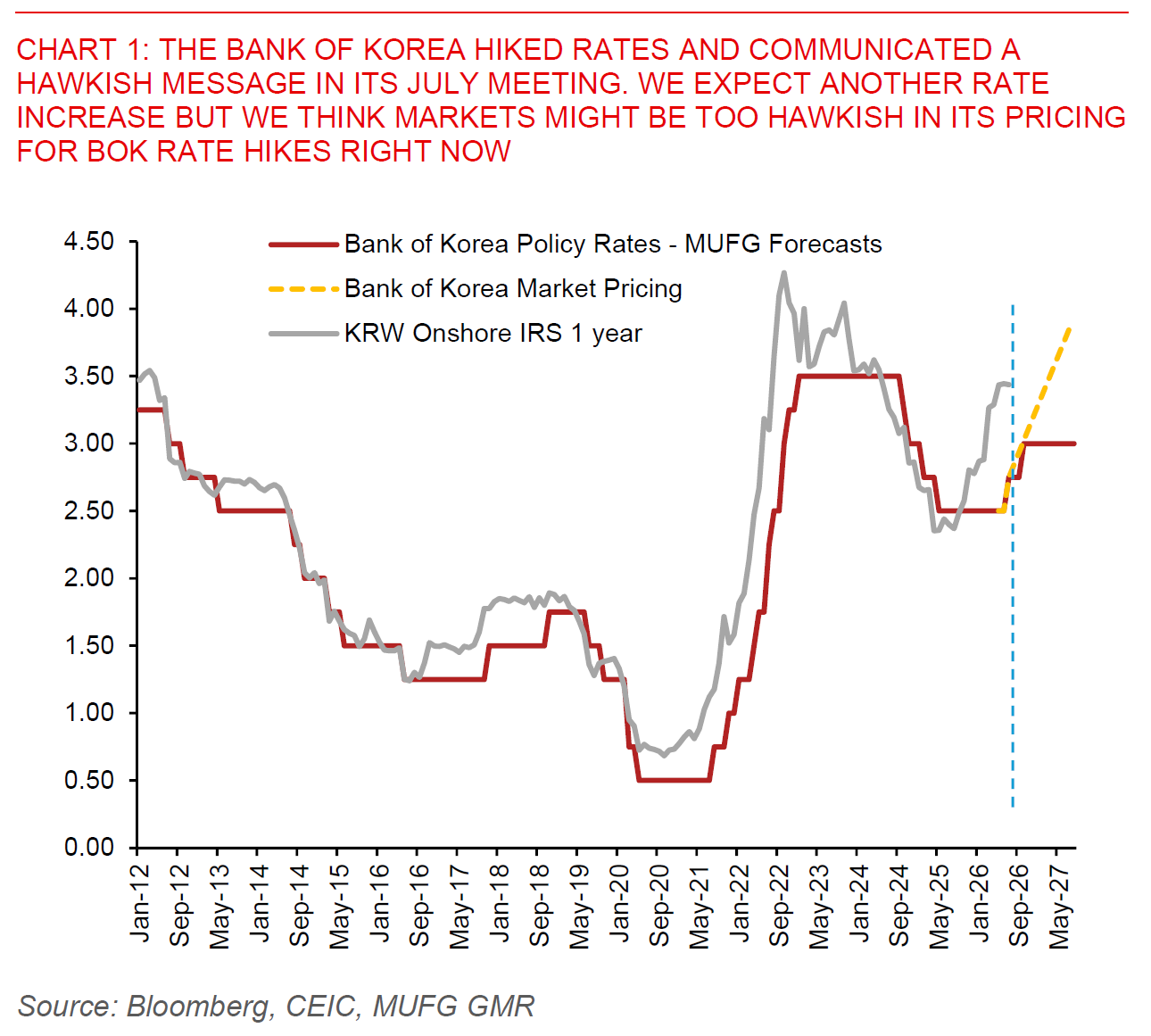

The Bank of Korea kicked off its rate hike cycle in its July 2026 meeting, raising its policy rate by 25bps, and as such bringing it to 2.75% from 2.50%. This move was widely expected by the market as a consequence of the hawkish communications in the May 2026 meeting including the raising of the BOK’s dot plots, the speech by Governor Shin Hyun-Song in June highlighting the need for further policy tightening driven in part by the sharp rise in South Korea’s nominal GDP and disposable incomes, coupled with macro data including exports which generally supported policy tightening.

The post-policy statement and press conference carried a hawkish tone pointing to further BOK interest rate increases as the path of least resistance. Nonetheless this was perhaps not hawkish enough relative to current market pricing, with KTB yields falling by around 15-30bps across the curve. First, the BOK in its statement highlighted the need for a policy stance consistent with further rate hikes, with the timing and pace of further increases to be determined. Second, the BOK sounded more confident of an improvement in domestic demand, with Governor Shin highlighting the AI boom and chip spillovers, including higher corporate profits and wages as key transmission mechanisms that will become more apparent over time. Third, while the headline inflation forecast remains at 2.7%, the BOK said core inflation is likely to be somewhat higher than expected and inflation to remain above target for a “ considerable time”, and with FX weakness also feeding into inflation.

From a macro perspective, our team does not expect the Bank of Korea to deliver as many rate hikes as are priced into the rates markets. Our base case has BOK skipping the August meeting and delivering another rate hike in 4Q2026 bringing the terminal rate to 3%, with one more rate hike possible in 1Q2027 if domestic demand spillovers prove stronger than we anticipate. Importantly, our expectation is lower than what markets are pricing right now, given at least 3 more BOK rate hikes expected by the rates markets over the next 12 months, with 1 year IRS at around 3.43% and 1y1d forward rates at 3.80% for instance.

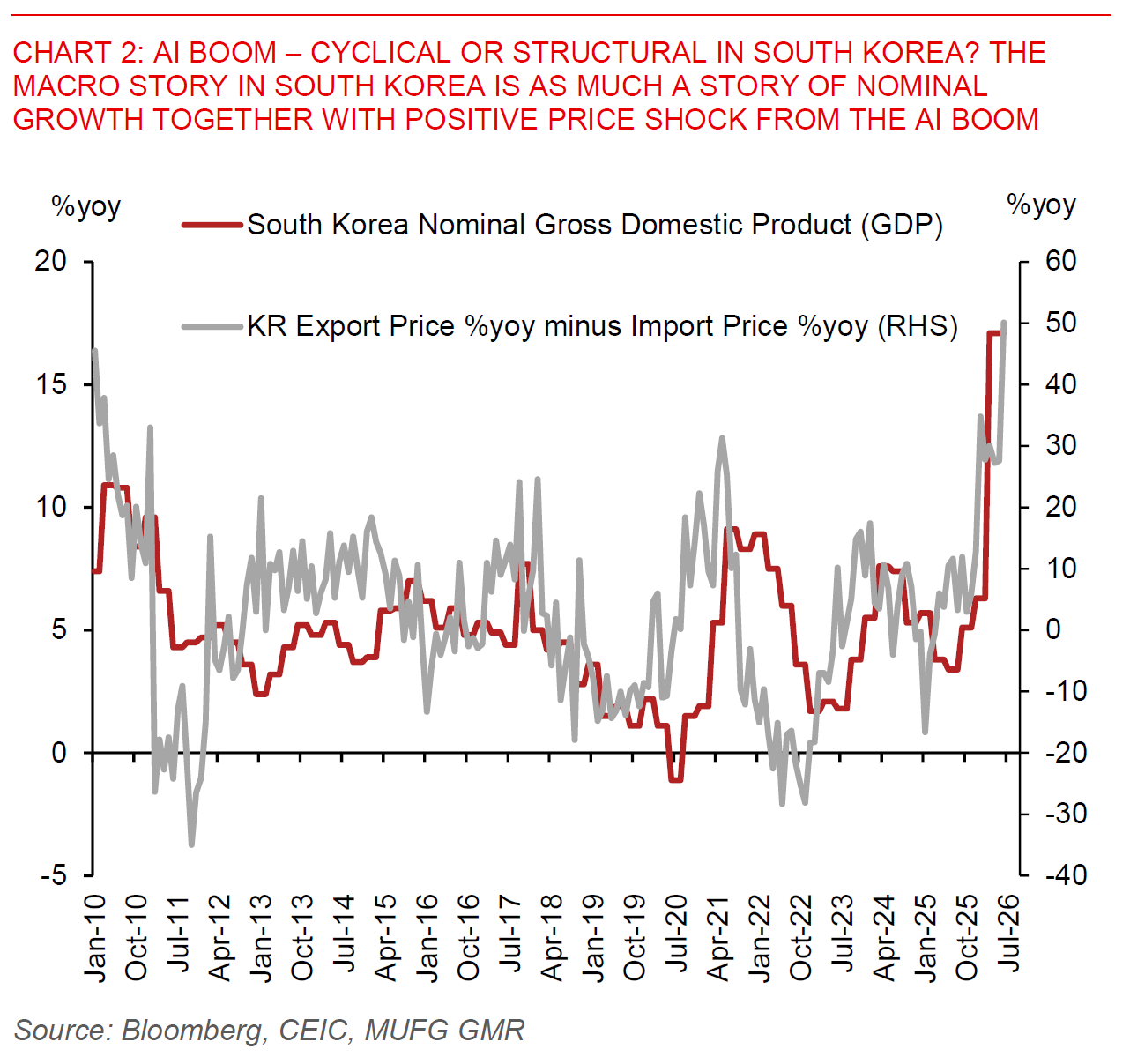

We would however caution that there is much we do not quite know right now about the AI boom’s impact to South Korea, including whether the memory cycle is structural or cyclical, how long this will extend, and the magnitude of the positive shock. To put things in perspective, South Korea’s export prices rose 71%yoy in the latest print, far outweighing the rise in import costs from oil prices, while with that nominal GDP rose by an absolutely massive 17%yoy. BOK Governor Shin said as such, reiterating that the AI transmission mechanism for Korea is most importantly a nominal growth story (more so than a volumes story), together with a massively positive terms of trade shock with export price increases outweighing import price increases. With stronger nominal GDP leading to stronger corporate profits, and some second-round effects such as higher tax revenues and the government possibly spending some of this additional tax income with the lagged impact of wealth effects to households, the BOK is essentially telling us that higher interest rates in South Korea is the path of least resistance.

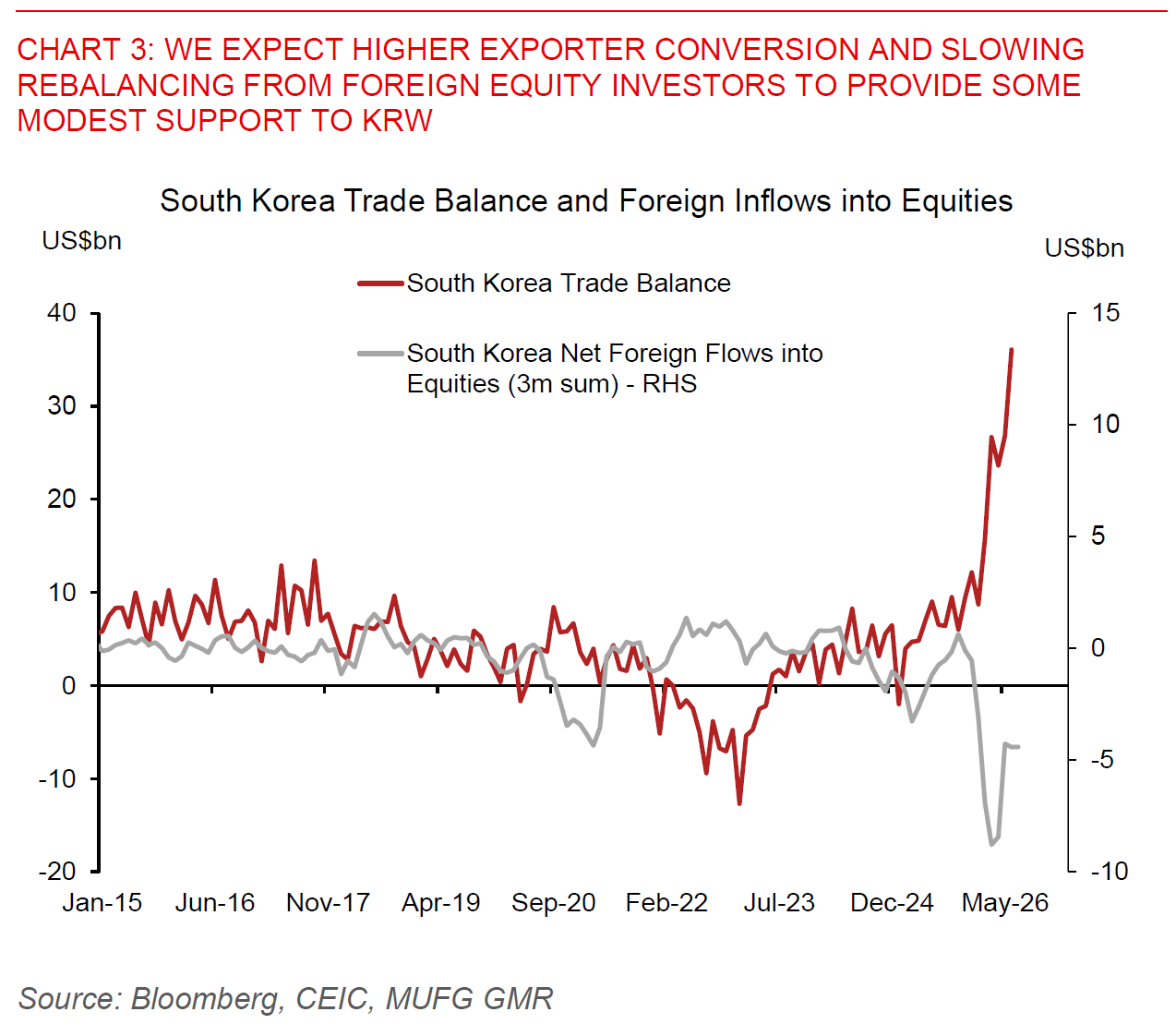

From an FX perspective, we continue to be biased to see some modest appreciation in KRW moving forward, especially given how weak KRW has already been so far. Higher BOK rates and with that rate differentials can and will matter for USD/KRW but we note that the FX flow picture is probably more the important FX driver. USD/KRW has moved towards the 1480 levels from the highs of 1560, driven by flows from SK Hynix’s ADR, increasing exporter conversion, coupled with perhaps a slower pace of index and stock rebalancing by foreign equity investors. We think the latter two should continue, but we might start to see the positive impact from SK Hynix’s FX conversion slow in August.

Putting it altogether from a strategy perspective, we would as such look for opportunities to receive Korean rates and go long duration on KTB bonds over time, and to also short USD/KRW on bounces. We would probably characterise our view on KRW rates as neutral, and note that it is a fool’s errand to receive rates well before the last rate hike and with BOK still remaining quite hawkish. Nonetheless, with quite a bit already in the price (3-4 hikes), we think the risk reward may tit towards rates going lower over time. From a KTB perspective, higher tax revenues may mean that that additional KTB issuance will be limited, but we would caution the government also has plans to push out more spending plans and as such this would be a key offset to bond issuance. From an FX perspective, KRW has been quite weak for some time, and we think moving forward we could see some slowing in stock rebalancing by foreign equity investors with exporter conversion helping. We are forecasting USD/KRW at 1460 over the next 12 months.