Ahead Today

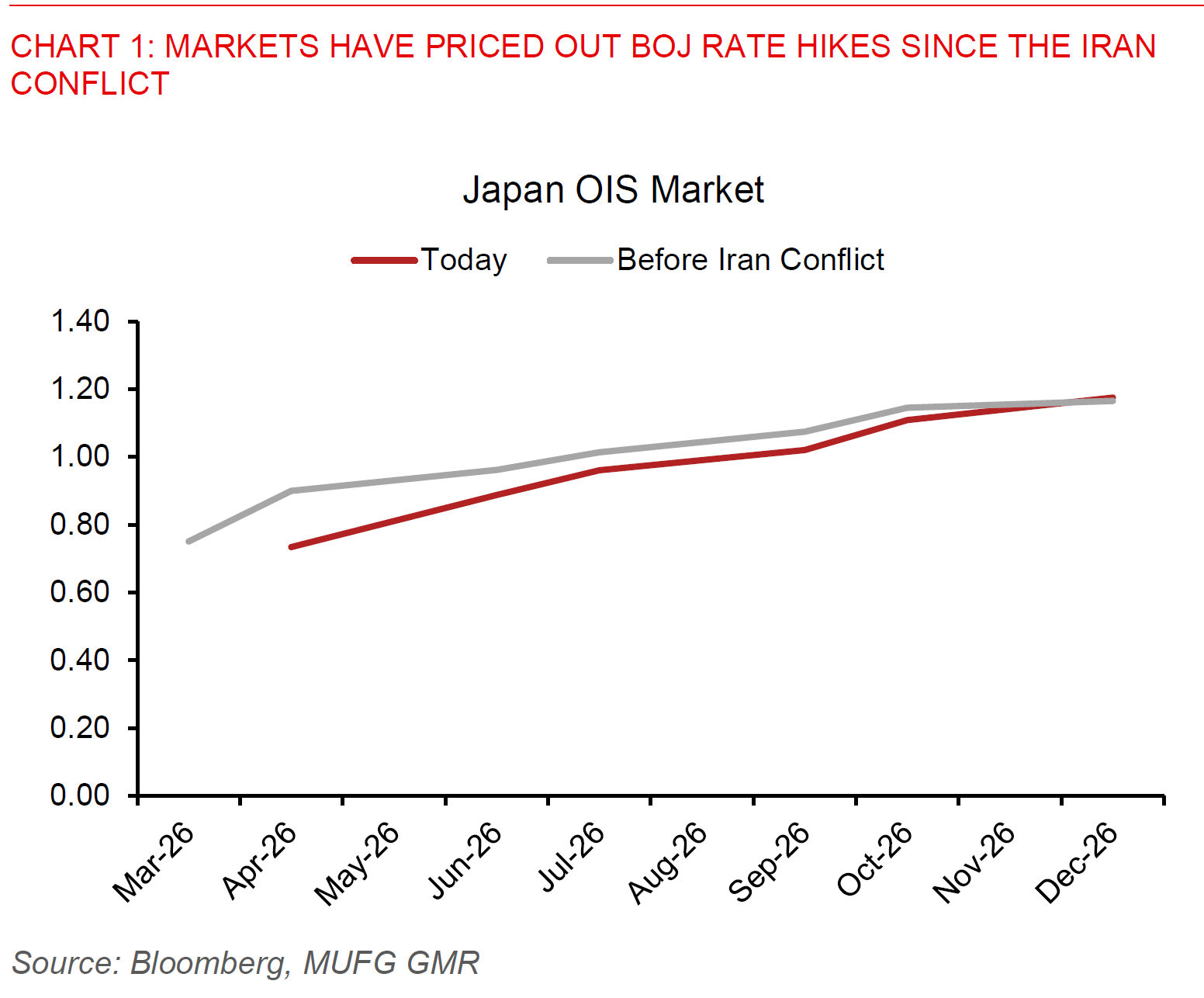

G3: Bank of Japan policy

Asia: Hong Kong Trade, India Industrial Production

Market Highlights

The Dollar weakened slightly and risk assets were mixed, as markets digested recent developments in the US-Iran negotiations and ahead of key global central bank meetings including the Bank of Japan later today. In particular according to news reports Iran submitted a proposal that would push the discussion on the nuclear issue to a later date, while including other details such as ending the naval blockade by the US, agree to a new legal framework for traffic going through the strait, and guarantee no future military action against Iran. The US administration were discussing Iran’s latest proposals but maintained “red lines” on any deal to end the eight week war, including preventing Iran from obtaining a nuclear weapon. Overall, beyond the noise and many comments by Trump, the big picture to us is that Trump wants a deal and that the appetite for further military action by the US is low, both because the mid-terms are around the corner, and also because munitions in the US military have likely been depleted quite substantially already. We as such think that de-escalation remains a base case, but the left tail risk remains meaningful and as such hedging some portion of risk remains quite a sensible policy moving forward.

The key event today is the Bank of Japan policy meeting. The OIS markets have already priced out a rate hike for the April meeting and consensus and ourselves are also expecting no change in rates by the BOJ. What’s more important for markets will be the communication on the path forward and also the tone whether hawkish or dovish. Overall, we pencil in a rate hike by BOJ for June, which in the context of the OIS markets pricing in around 62% probability of a rate hike that meeting should provide some support for JPY moving forward. Nonetheless in the interim we could certainly get some volatility perhaps with USD/JPY peaking above 160 if the BOJ communication proves more dovish than expected.

Beyond that, China announced that it has blocked Meta’s acquisition of Manus AI, and is the first instance we know of that imposes foreign investment restrictions on critical technologies including AI. While Manus’ technology is not cutting edge by any means today, given that it is a wrapper around existing models and many key AI companies are already developing agentic workflows and products, what it does signal is a more controlled environment by Chinese authorities on sectors deemed to be of national interest, including in areas such as AI, robotics, and perhaps even biopharma/biotech. We don’t think this will derail the upcoming Trump-Xi summit given that it is low in the priority in the grand scheme of things. Nonetheless, the overall direction of the US-China relationship contains many risks including the ongoing discussion of the MATCH Act on global restrictions on semiconductor tools on countries such as the Netherlands and Japan, coupled with China’s increasing use of offensive trade and industrial tools to protect its interests – perhaps understandably so – including recent State Council Orders no 834 and 835.