Ahead Today

G3: US ISM Services, Fed Beige Book

Asia: Vietnam Trade balance, Vietnam CPI, China Ratingdog PMI

Market Highlights

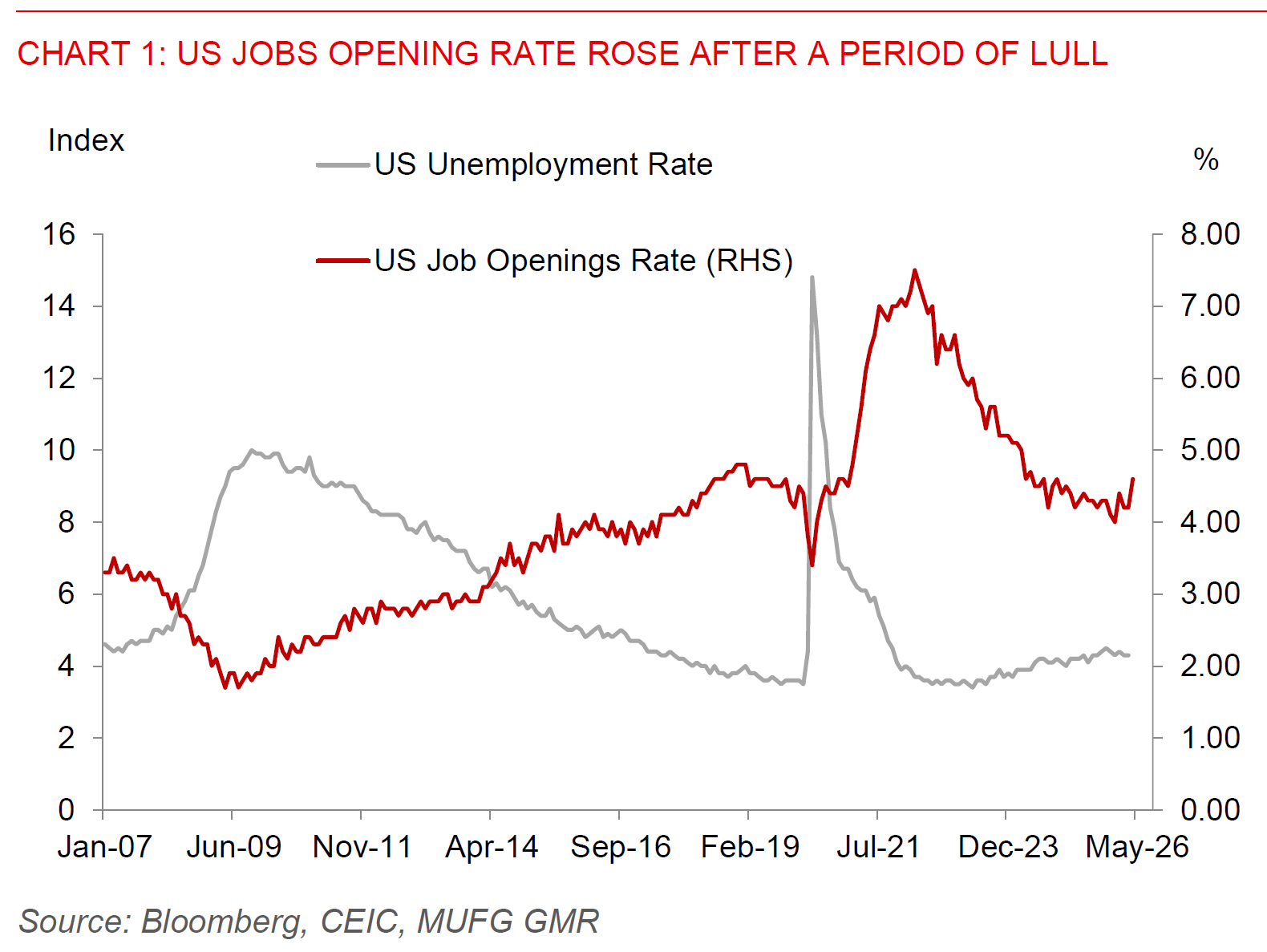

US labour market data came in stronger than expected, and with that US yields ticked higher while the Dollar was stronger as a result as well. In particular April job openings rose to 7.62 million, above the consensus of 6.87 million and the highest since May 2024. The details were still suggestive of a labour market perhaps having both cyclical and structural headwinds including on the potential impact of AI, with quit rates remaining quite low below 2%. Nonetheless, what’s interesting is that jobs opening rates rose to 4.6% from 4.2% previously, and Governor Waller has in the past mentioned that jobs openings rate can be a key measure to anticipate tipping points between an acceleration in unemployment rates with 4.6% a key level to watch. Overall, it does point to a FOMC and Fed which might find it more difficult to justify rate cuts at least in the near-term, notwithstanding new Fed Chair Kevin Warsh’s proclivity to cut rates and focus on trimmed mean inflation and the productivity impact of AI. We already have some FOMC member turn somewhat more hawkish on the outlook for US rates, and with the committee seemingly more divided perhaps doing no harm is the best course of action for a policymaker in the near term.

With that context in mind, the US ISM Services data and Fed Beige Book out later today, coupled with the US Non-Farm Payrolls later this week will probably be more important than usual in gauging turning points in both US rates, the US Dollar, and with that Asian currencies as well. We already have the likes of USD/JPY reaching shy of the 160 mark, and we wouldn’t be surprised if the Finance Ministry jawbones the currency and maybe intervenes once again at those key levels. Nonetheless, the fundamentals as mentioned about sticky US yields, but more importantly coupled with still low Japan real yields and fiscal policy turning more expansionary remain the key drivers. Ultimately we think the BOJ has to act and hike rates for the trend in USD/JPY to change, and BOJ Governor Ueda’s speech later today could be important in that regard in signalling the path forward.

Meanwhile in Asia, the theme of AI versus Hormuz remains, and as the April trade data in totality across all countries show the phenomena of “first come first serve” – countries getting their hands on as many barrels as possibly from sources such as Russia, US, and even Brazil and Angola. Indonesia’s trade numbers released yesterday showed a sharp drop in the trade surplus from US$3.3bn closer to US$100mn, quite a large chunk of which was driven by a rise in oil imports by around US$1.6bn. Some of this may be explained by seasonal factors given shifting timings of holidays, but if one puts in the broader context of how USD/IDR has already traded this makes sense with both local factors such as domestic policy and fiscal uncertainty combining with at least in the near-term a decline in support from the trade balance and current account. We think moving forward that higher commodity prices more generally should help IDR and the markets seem to already be quite bearish, but for things to turn greater policy certainty including on fiscal policy and the export agency for commodities probably needs to happen.