Ahead Today

G3: US S&P PMI

Asia: Singapore CPI, India PMI, Taiwan export orders

Market Highlights

Talks between the US and Iran seem to have progressed quite well, with US Vice president JD Vance describing the first round of negotiations as “very, very good”, and said Iran had agreed to allow nuclear inspectors back into the country – although this claim was subsequently disputed by Iran. Overall, the US also issued a 60-day license allowing Iran to sell oil in the international market, giving Iran some economic benefits as both sides continued talks for a permanent peace deal.

Overall, our base case is that the US-Iran deal and de-escalation sticks, even as there is some risk around how Israel will respond moving forward and also as we think the timeline for negotiations will likely stretch beyond the stated 60 days. There is certainly an incentive for Trump to press ahead with a deal, but we think more importantly, there are incentives not only for Iran but also the Gulf states to keep both parties at the table. While there were certainly diverging views on the approach to Iran initially within the GCC especially between the UAE and Saudi Arabia and Qatar, what seems clear to have emerged is now a rational response to a new regional order that is likely to emerge in the Middle East – certainly replacing the previous model of US security.

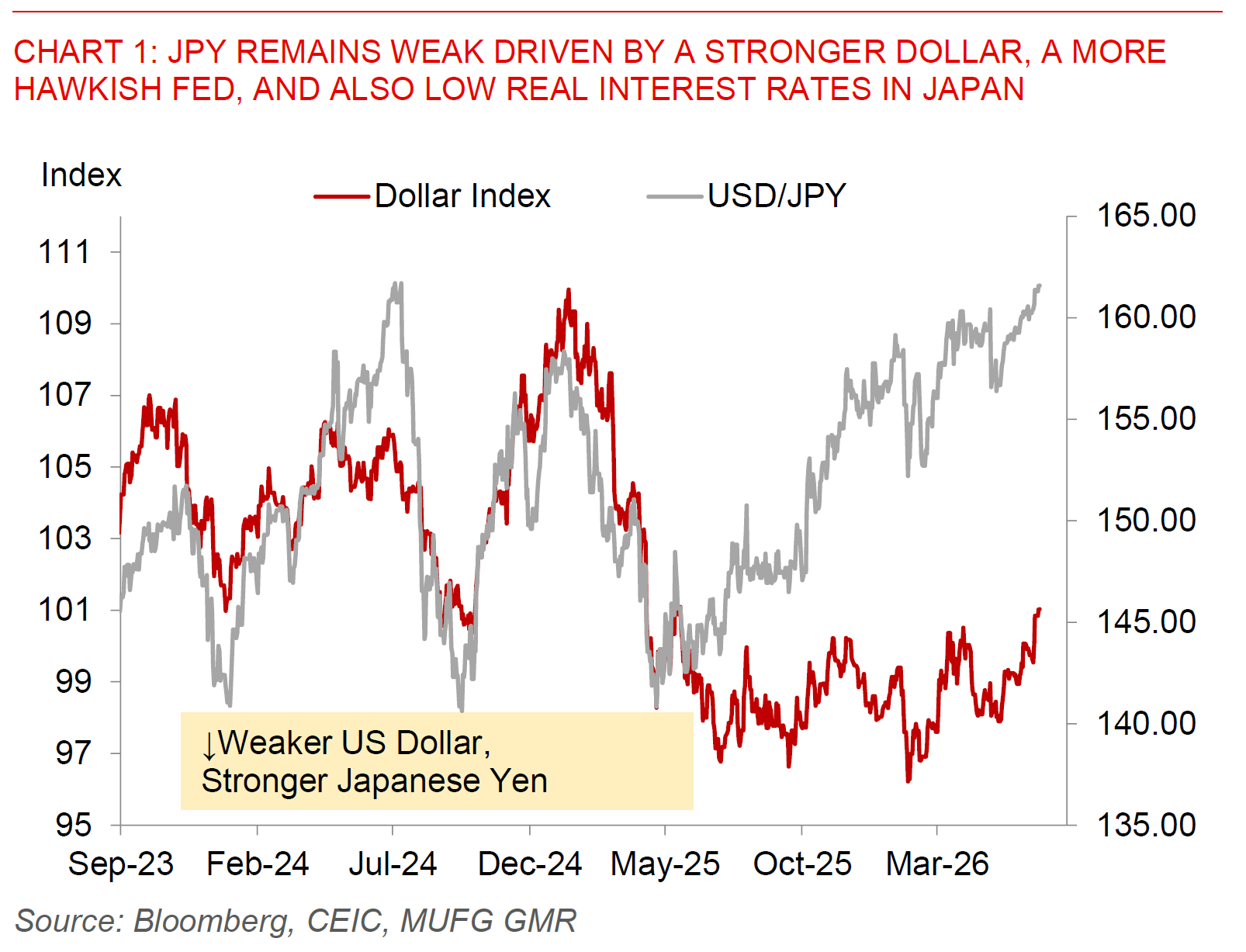

From a markets perspective, the Dollar continues to edge stronger with EUR/USD falling closer to the 1.14 levels and USD/JPY twitching closer to the 162.00 levels. With that Asia currencies have generally been modestly weaker but we note the moves have been orderly with risk sentiment and lower oil prices key drivers supporting FX and rates markets in our region.

The Japanese Yen in particular saw a sharp drop intra-day from 161.93 to the 161.00 levels, before bouncing up to 161.60. It’s unclear whether this was driven by actual intervention, but what moved markets was news reporting out by NHK that Japanese Finance Minister Satsuki Katayama held an online meeting with US Treasury Secretary Scott Bessent together with Japan’s top currency official Atsushi Mimura, with officials potentially discussing views on the currency. Overall for USD/JPY, we think ultimately the fundamentals of low real interest rates vis-à-vis the US have to change for a durable shift in the trends, and as such the Bank of Japan likely has to signal a more hawkish path together with some easing of expectations of a hawkish Fed right now. Our expectation is that the BOJ will hike rates at least once more this year by December with the risk tilted towards earlier hikes, but in the near time the bias seems tilted towards USD/JPY moving higher until we get better clarity on that front.