Ahead Today

G3: -

Asia: Malaysia Trade, Malaysia CPI

Market Highlights

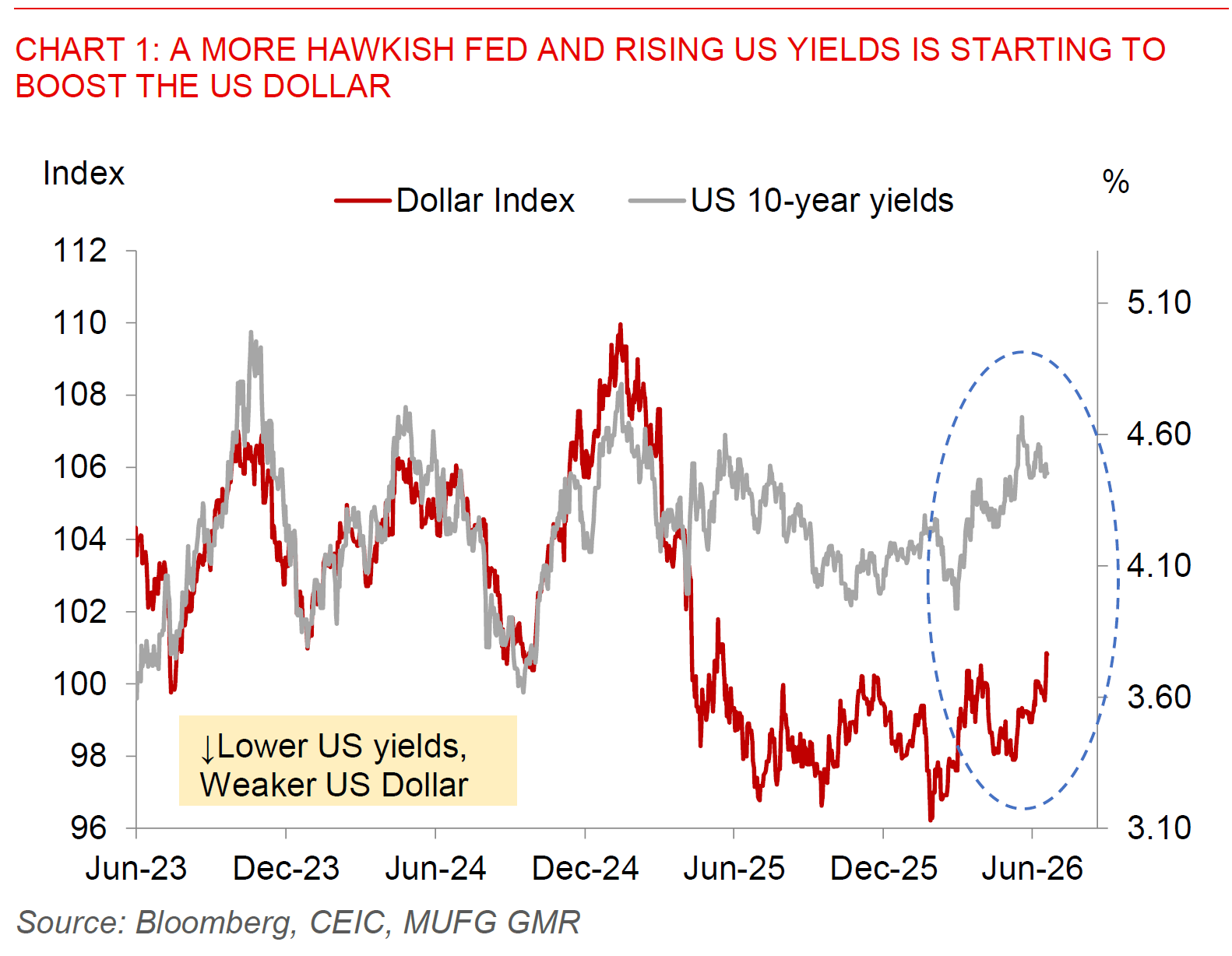

The US Dollar strengthened as part of a flow through from the hawkish Fed during Kevin Warsh’s first policy meeting as Fed Chair, but the overall move was orderly with a pickup in equities and risk. Some of this may reflect offsetting factors such as an expected reopening of the Strait of Hormuz with the US-Iran deal, and with Brent oil falling below US$80/bbl. From an FX perspective, in combination we saw the likes of EUR/USD falling below 1.150, USD/JPY rise above 161 levels raising some risks of FX intervention, but with some modest outperformance in the likes of oil importing currencies such as INR and PHP driven in part by lower oil prices. Moving forward, much will also be dependent on how the market perceives the Fed under Kevin Warsh. Given the changes he is likely to bring to the Fed in terms of communication and reduced emphasis on forward guidance, we could well go back to an era of higher rates volatility, with markets finding it more difficult to price the Fed’s reaction function including around key datapoints such as the non-farm payrolls. In addition, his taskforces could provide some justification for a fundamental reshaping of the Fed.

Across Asia, we saw central bank decisions from the Philippines, Indonesia and Taiwan. We saw the Philippines and Indonesia hike by 25bps, while the CBC remained on hold. Overall, with the earlier spike in oil and energy prices, the possibility of second-round effects to inflation, coupled with spillover effects to other transmission channels such as a weaker FX, several central banks including the Philippines and Indonesia have been raising rates to help manage inflation expectations. Of course it is not just about global factors, and in the case of Indonesia for instance, the fiscal dynamics, domestic policy uncertainty and with that also the upcoming MSCI market review continue to be key drivers of the Indonesian Rupiah. Just this morning, MSCI highlighted concerns over market accessibility in Indonesia, downgrading Indonesia’s information flow criterion to negative. This comes ahead of a key market status review report out next week on 23 June on whether MSCI will downgrade Indonesia from emerging markets to frontier market, a decision which could result in further portfolio outflows.