Ahead Today

G3: US JOLTS Jobs opening

Asia: Indonesia trade, Indonesia CPI, India Current Account

Market Highlights

A key driver across all markets remains the negotiations around US-Iran conflict and whether there is a deal reached. Over the weekend, the two sides exchanged revised proposals but failed to reach a breakthrough, with renewed military strikes — the US conducting what it described as "self-defence" strikes on Iranian radar and drone facilities, and Iran's IRGC targeting a US air base — further straining the fragile ceasefire. On Monday, Iran's semi-official Tasnim news agency reported that Tehran had suspended negotiations via intermediaries, citing Israel's escalating offensive in Lebanon. Brent crude surged as much as ~6% intraday to near $97/barrel before closing around 4% higher. What helped markets recover as we speak this morning was announcements by Trump that in his conversations with both Israel Prime minister Netanyahu and Hezbollah that they both agreed to stop shooting, although Israel’s leader did not describe it in such sweeping terms.

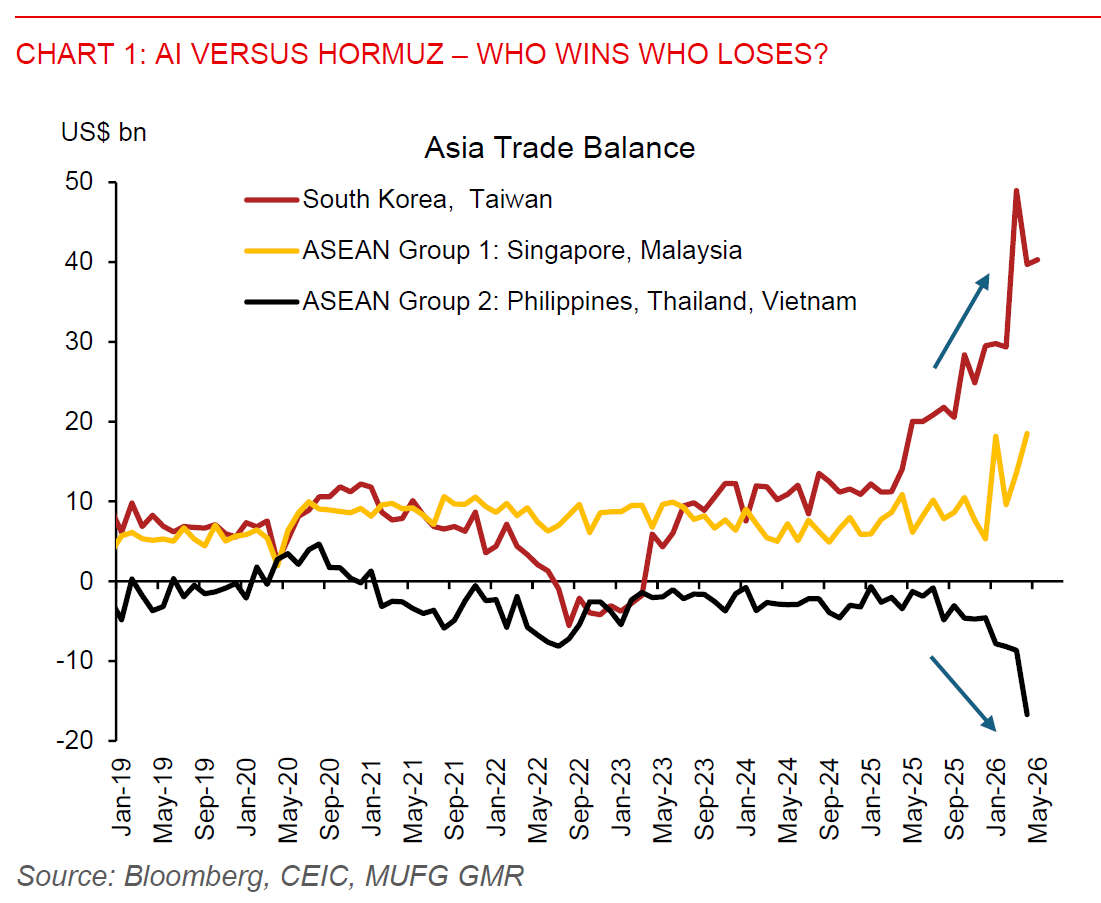

While Asia’s markets continue to gyrate around the rollercoaster of US-Iran negotiations, what's important to note is that the positive impact of AI has offset the negative spillovers from the Strait of Hormuz for some Asian markets – in particular South Korea and Taiwan, and to a smaller extent Singapore and Malaysia. The trends are most evident in South Korea’s case, given the surge in agentic AI and the supply side bottleneck especially in the memory space. In other words, the constraint now is not demand at least for now from an infrastructure build-out perspective – the constraint is the supply of chips and in particular memory.

What’s notable for South Korea were hawkish comments by BOK Governor Shin Hyun-song, which essentially seemed like he was prepping markets for a July rate hike. In particular, he said that strong semiconductor exports have boosted growth rates and eliminated the dilemma for BOK around monetary policy, with many indicators including household debt and exchange rates pointing in the same direction. Comments around strong nominal GDP growth and also the sharp improvement in terms of trade were also interesting, and pointed to a focus by the central bank on prices and not just volumes. With the inflation numbers coming in stronger than expected at 3%yoy and exports in May on a working day adjusted basis coming in at a phenomenal 60%yoy, it does seem like it’s still an environment for South Korea rates to remain sticky moving forward.

What’s diverging is also from an FX perspective, with the South Korean won not responding so far or benefitting from these signals. On our end, we think that will change and KRW is one of our top picks from an FX perspective moving forward, given cheap valuations, a more hawkish BOK, the gravity defying exports, a likely further improvement in the current account surplus, coupled with improvement in earnings expectations likely to offset resident outflows over time. We see USD/KRW moving towards the 1400 level through the next 12 months.