Commodities pare back their post-war gains as the geopolitical risk premium unwinds (for now)

Global commodities

Our thoughts continue to be with those affected by the ongoing conflict in the Middle East. Wars have a historical habit of yielding unintended consequences. Yet, global markets remain inclined not to rush to judgement. The aggregate Bloomberg commodity (BCOM) index has pared almost all its gains, led by energy and base metals, since the start of the war on 7 October as the geopolitical risk premium unwinds with Israel seemingly recalibrating its ground invasion of Gaza. Yet, we would stress that these are still early days and the crisis facing Israel is unique with trajectories not fully aligned with previous calculations in times of conflict – fat tail risks of containment or conflagration remain on the table. Though with no clear signs the war will spiral, attention is returning to volatile swings in the US bond market and the broader fragile state of the world economy, that is unsettling investors. Manufacturing remains in a sustained funk, reinforced by the global PMI manufacturing index printing firmly under the 50 threshold that separates expansion from contraction since September 2022. This has been joined by the global services PMI has also come down since the mid-year surge that broke out as core central banks slowed/stopped their tightening cycles. On net, the comprehension of geopolitical angst as a historical constant steadies global markets in a storm and the message the markets are sending (for now) is that worst case scenarios of a regional conflagration will not come to pass.

Energy

Notwithstanding the war risk premium subsiding – alongside acknowledging that no barrels to market have been impacted since the conflict between Israel and Hamas started on 7 October – upside oil risks abound. As we highlighted last week, risks remain on how the US can skilfully navigate pressure to tighten the enforceability of its sanctions on Iranian barrels without (i) antagonising (politically) China’s growing appetite for discounted Iranian crude, and (ii) exacerbating (economically) upside pressure on US gasoline prices that lower Iranian crude exports may cause (see here). Meanwhile, in natural gas markets, Egypt LNG exports now appear impacted (albeit negligibly) by the Israeli Tamar field shutdown, although this has been more than offset by this month’s start-up

Base metals

Copper (the bellwether of the global economy) remains an accordion market. It remain mired in near-term surpluses and prices weakening as the bellows expand. Yet, later comes the inevitable squeeze as the bellows get compressed. Brace for further downside but position for the reversal.

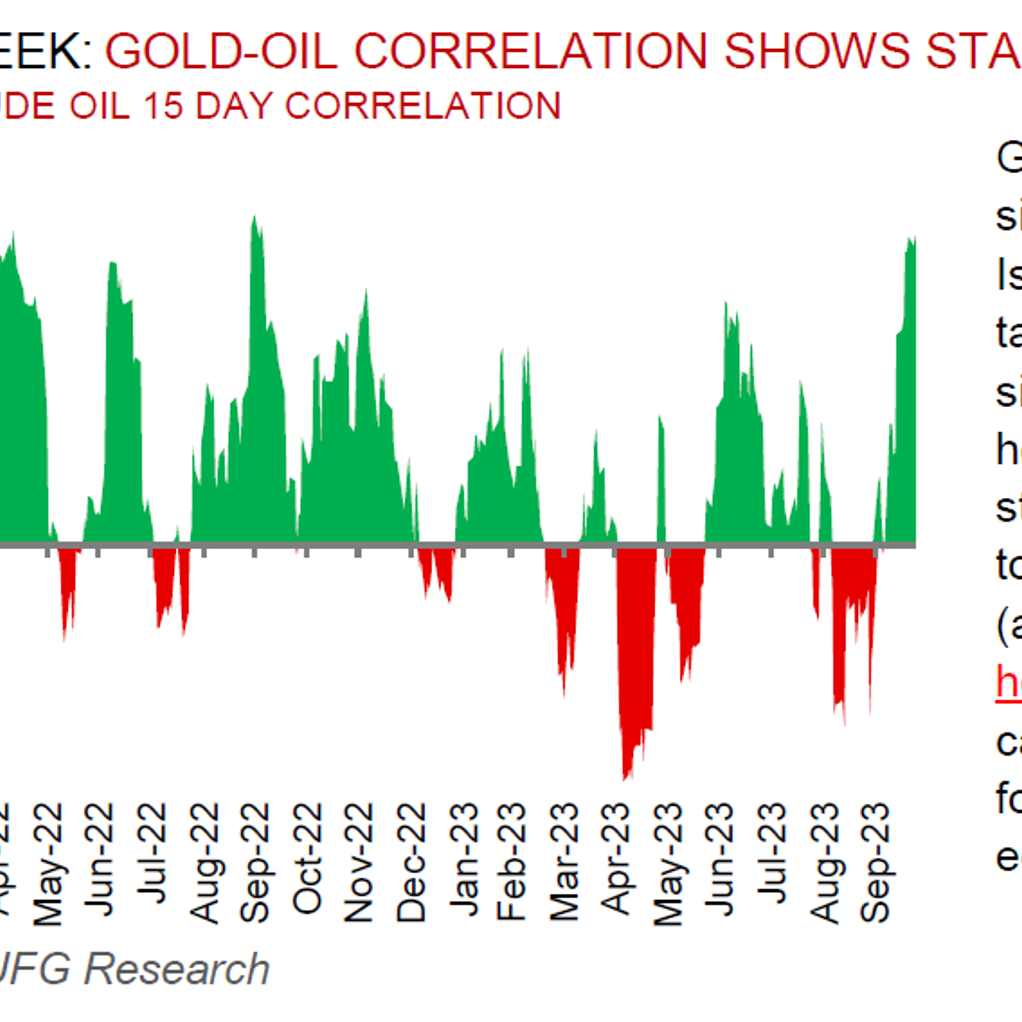

Precious metals

Gold prices rallied towards five-month highs amidst escalating geopolitical risks in the Middle East with the estimated open interest value across precious metals rising by over USD10bn last week. For current pricing to persist, geopolitical tensions need to remain, or real yields need to move lower.

Bulk commodities

Iron ore is retracing some lost ground as the Chinese government prepares for additional sovereign debt issuances as part of efforts to stimulate infrastructure spending. Meanwhile, global coal fundamentals remain balanced, with the downside risks to China imports offset by upside risks to India imports.

Agriculture

New York cocoa has surged to the highest level in 44 years as global shortages is pushing up prices. Going forward, apprehensions over crops as the El Nino weather pattern strengthens may keep cocoa prices higher into the 2024 season. Exacerbating the situation are ESG considerations, coupled with aging trees’ susceptibility to pests which could curtail mid-term production growth.

Core indicators

Price performance and forecasts, flows, market positioning, timespreads, futures, inventories, storage and products performance are covered in the report.