USD100/b oil reawakens stagflation trepidation

Global commodities

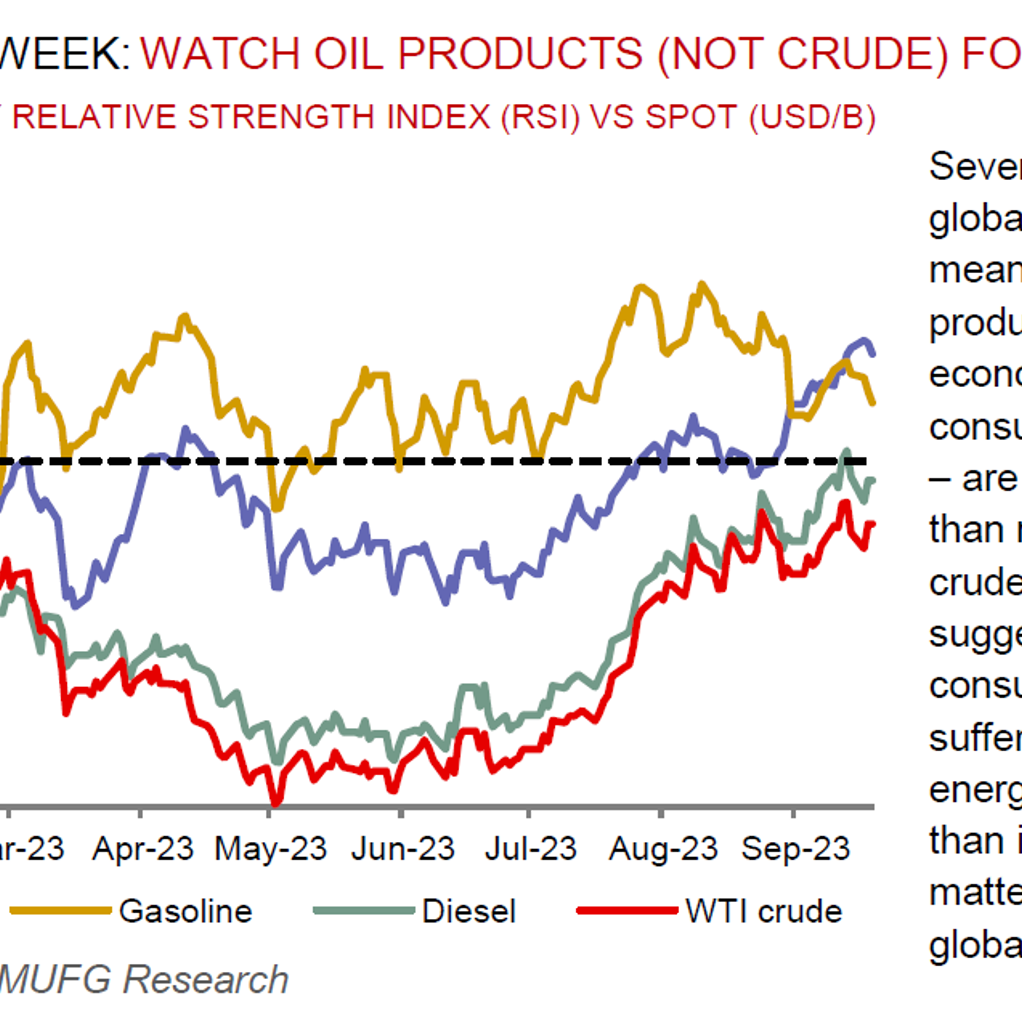

As oil prices continue their relentless rally higher, conversations in the energy market are increasingly fixated on when, rather than if, prices will return past to the coveted USD100/b threshold. Given the tightness in the global refinery space (see here), purchasers of petroleum products (gasoline, diesel, jet fuel) – what the real economy is exposed to – may begin to feel the pinch. With it, the reverberations on global growth may become more pronounced with rising energy costs fanning the flames of global inflationary pressures once again, complicating the task of central bankers and increasing the probability of higher for longer rates. What is clear is that the surge in energy prices is threatening the soft landing narrative, keeping inflation high even as growth slows with stagflation trepidation now top of mind. What do you want to own in such a stagflationary environment? Commodities – as real physical assets – have historically proven to be the ideal hedge offering high returns, low correlation with other asset classes and protection from inflation (see here and here). At stagflation’s core is severe limitations on supply which the market has to rebalance through demand destruction (as prices in the economy keep rising but economic activity does not). Critically, we are convicted that demand weakness can relieve the symptoms of underinvestment – namely, commodity inflation – but cannot cure the underlying illness of inadequate production capacity. This strikes at the heart of our decades-long supply-constrained supercycle thesis (see here).

Energy

After its blistering climb, oil’s rally has hit the pause button, as the Fed’s higher for longer signal eclipses declines in stockpiles. Heading into the FOMC meeting, crude’s technical metrics (both the RSI and MACD) had already suggested a breather was on the table. While we believe that most of the rally is behind us, we do not rule out a transitory breach for Brent crude north of USD100/b given how deep the market deficit is, alongside severely depleted inventories. Though we still hold our conviction that such a move above USD100/b will not be sustainable (see here and here). Meanwhile, in global gas markets, high frequency LNG data continue to point to normal loadings out of Australia despite a temporary 20% production outage at the 8mtpa Wheatstone LNG export facility last week, suggesting no impact from the ongoing strike at the Gorgon and Wheatstone export facilities.

Base metals

Base metals depressed equilibrium continues with strong China green transition demand, supporting import pulls, offset by continued deterioration in developed markets demand with a rates-tied construction downturn and supply chain destocking still domineering headwinds across the space. As alluded to last week, the key risk going forward is that the duration of the manufacturing downturn extends into 2024, in part owing to the piecemeal pace of Chinese policy easing, alongside the industrial supply chain reverberations from higher for longer rates across developed markets.

Precious metals

Gold has been holding steady in recent trading sessions. Whilst the Fed held rates as widely expected on 20 September, swaps markets are pricing in elevated rates across major developed markets given the higher for longer market narrative. As a non-yielding asset, gold is having to compete for a place in portfolios (less of an issue when bond yields are low, but more challenging as yields rise).

Bulk commodities

China’s cutting banks’ reserve requirement ratio (RRR) is being felt in iron ore markets, with prices hitting five month highs, as steel mills ramp-up production amid a seasonal pickup in construction after the summer. The iron ore market is also finding momentum by Chinese authorities’ support for the property sector through the easing of buying restrictions. We still conviction to remain cautious on iron ore with micro conditions offering prospects of a softening turn with the surplus trajectory expected in the remaining months of 2023 (see here).

Agriculture

In its latest report, the European Commission said that the EU’s soft wheat exports for the ongoing season stood at 6.32MT as of 17 September, down 27% y/y. The major destinations for these shipments were Morocco, Nigeria, and Algeria. As for corn imports, these stood at 3.3MT over the same period, down 44% y/y. Last season the EU saw stronger corn imports due to a poor domestic crop.

Core indicators

Price performance and forecasts, flows, market positioning, timespreads, futures, inventories, storage and products performance are covered in the report.