Parameterising geopolitical scenarios and energy prices

EHSAN KHOMAN

Head of Commodities, ESG and

Emerging Markets Research –

EMEA

DIFC Branch – Dubai

T:+971 (4)387 5033

E: ehsan.khoman@ae.mufg.jp

RAMYA RS

Analyst

DIFC Branch – Dubai

T:+971 (4)387 5031

E: ramya.rs@ae.mufg.jp

MUFG Bank, Ltd.

A member of MUFG, a global financial group

Global commodities

Our thoughts continue to be with those affected by the ongoing conflict in the Middle East. Given still fat tail risks of containment or conflagration miring the Middle East, we parameterise through scenario analysis the reverberations of geopolitical scenarios on both Brent oil and European natural gas (TTF) prices. At the outset, it is imperative to contextualise that energy (and broader commodity) markets are physical markets driven by volume (unlike financial assets such as equities, bonds, credit and debt, driven by dollars). This matters profoundly in understanding price dynamics as spot physical commodity assets only depend on the prevailing level of demand and supply. With this in mind, our base case (70% probability) remains for a “contained war” between Israel and Hamas. In such a situation (that we are witnessing today), oil supply (that has critically not been affected thus far), we are witnessing only a mild USD3-5/b rise to ~USD85b that is being driven by geopolitical risk premia, whilst the shutdown of the Israeli Tamar gas field (which has lowered physical global LNG supply by ~1.5%) has seen a substantial ~30% increase to ~EUR50/MWh. An escalatory “proxy war” that we define as a significantly higher intensity of skirmishes than pre-conflict norms (25% probability) would see, according to our modelling analysis, Brent oil breach USD100/b whilst European TTF would rise north of EUR85/MWh. We also consider a severe “direct war” scenario between Israel/US and Iran with regional conflagration, that draws parallels to the 1990 Gulf War, which we believe could see Brent oil well north of USD120/b and European TTF prices rising above EUR180/MWh.

Energy

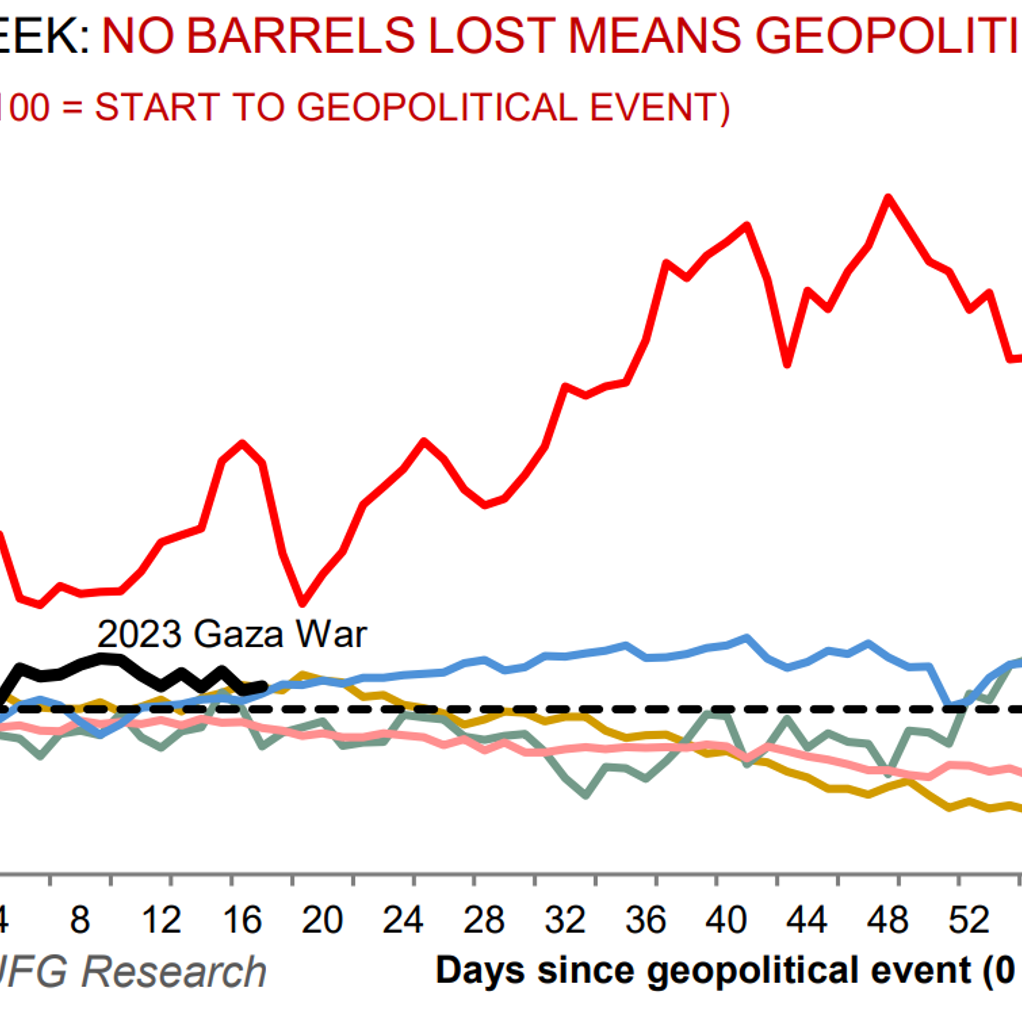

Notwithstanding no physical crude oil barrels being lost to market, the Israel-Hamas war continues to test trader’s nerves with tensions being played out in the derivatives market. Whilst investor positioning for geopolitical shocks is common practice, the lack of oil price follow through reinforces the message that markets are (for now) deeming worst case scenarios of a regional conflagration will not come to pass. Meanwhile, US natural gas (Henry Hub) prices have climbed to nine month highs as forecasts for colder-than-normal weather for this time of the year, is boosting expectations for higher demand for heating, power and feedgas for LNG exports.

Base metals

Base metals remain on the back foot as apprehensions over rising stockpiles and weakening demand come to the fore. The soft China manufacturing PMI reading for October will only add to the headwinds, offsetting the transitory lift that came from the latest round of Chinese stimulus. In particular, copper – the bellwether of the global economy – is now seen three consecutive monthly declines (longest losing run this year).

Precious metals

The speed of the geopolitical-induced rally in gold has sharply inverted the call skew in the options market driven by upside demand. The rally has caused upside volatility to a much more elevated degree than was implied by the skew as tail risks were priced. Call volatility remains elevated, which may see interest from those looking to lever the skew, and are either bullish on gold or expecting a reversal.

Bulk commodities

Rising gas prices on the back of geopolitical tensions is beginning to trigger gas-to-coal fuel switching in Europe with coal back in the money. The economics of coal generation looks set to remain more favourable than gas throughout the winter, signalling an impending rise in coal-fired power. Meanwhile, with Europe’s natural gas inventories close to “tank tops” at 99% full, European energy companies are reportedly turning to Ukraine to park excess reserves ahead of the peak winter months.

Agriculture

Wheat prices have fallen to the lowest in more than two weeks as (i) a US dollar; (ii) improving conditions in some key growers; and (iii) undeterred Black Sea shipping, is bolstering the outlook for crops.

Core indicators

Price performance and forecasts, flows, market positioning, timespreads, futures, inventories, storage and products performance are covered in the report.