FX Daily Snapshot

- Mar 26, 2024

FX stability encouraged by expectations for synchronized central bank easing

CNY & JPY: Pushback against domestic currency weakness continues

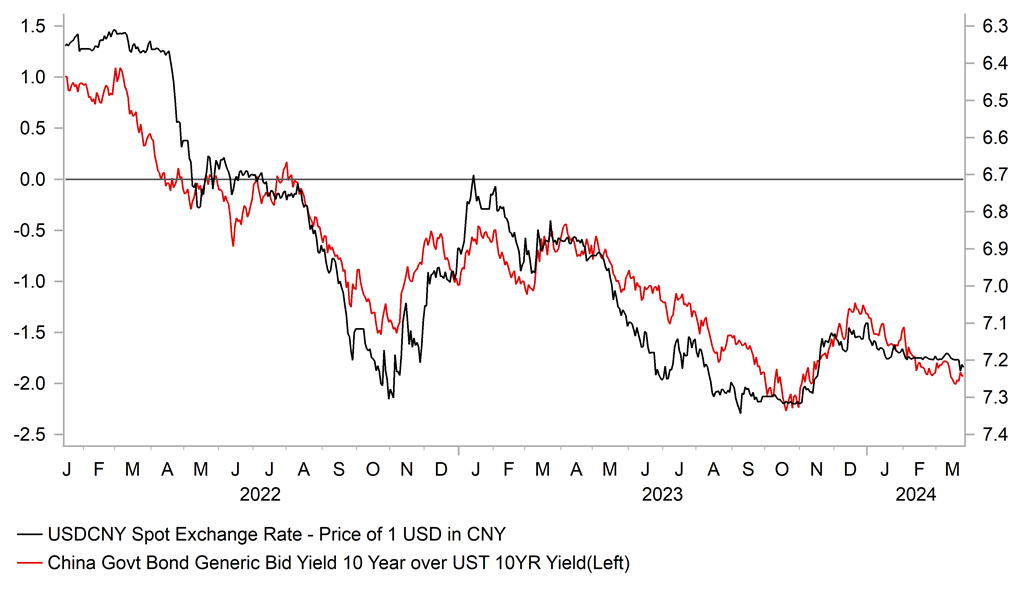

The major foreign exchange rates have remained stable during the Asian trading session after further pushback by Chinese and Japanese officials against domestic currency weakness. The PBoC set the daily fix for USD/CNY lower for the second consecutive day at the start of this week. The PBoC strengthened the fixing by 0.07% from Monday which was the most since 24th January which is helping to ease speculation that Chinese officials are becoming more tolerant of a weaker renminbi in the near-term. Despite the stronger fixes at the start of this week, USD/CNY has continued to trade above the 7.2000-level after breaking above on Friday for the first time since mid-November. Recent price action has increased the likelihood that USD/CNY will continue to grind higher back towards last year’s highs at just above the 7.3000-level amidst broad-based US dollar strength. Weakness in the renminbi has been encouraged as well by recent comments from the PBoC who have twice indicated this month that there is still room to lower the reserve requirement ratio. Market-based yields in China have continued to fall at the start of this year in contrast to the pick-up in US yields as Fed rate cut expectations have been pared back.

At the same time, Japanese officials have continued to voice more concern over recent yen weakness overnight which is helping to put a dampener on USD/JPY upside as the pair moves closer to the highs from recent years at just below the 152.00-level. Finance Minister Suzuki reiterated overnight that the Japanese government will take appropriate steps against excessive currency moves, without ruling out any measures. He noted that he was watching FX moves with a high sense of urgency, and that the exchange rate should move stably reflecting economic fundamentals. It follows the more robust warning over yen weakness yesterday from the Vice Finance Minister for International Affairs Masato Kanda that marked a clear step up in the level of verbal intervention from Japanese officials (click here). While verbal intervention won’t be sufficient to reverse the yen’s weakening trend on its own, it should at least help to slow the pace of further weakness as USD/JPY moves closer to the 152.00-level. The latest IMM positioning data from the week up to the BoJ’s latest policy meeting on 22nd March revealed that Leveraged Funds continued to hold elevated short positions that recently reached their highest level since 2018. Japanese officials have indicated concern that speculative yen selling has been mainly responsible for the move higher in USD/JPY over the past week and that it is not fully backed up by a change in fundamentals.

USD/CNY VS. LONG-TERM YIELD SPREAD

Source: Bloomberg, Macrobond & MUFG GMR

USD: Major central banks easing cycles are becoming more aligned

An important reason why the major currency pairs of EUR/USD, GBP/USD and EUR/GBP continue to trade within narrow ranges is the recent lack of monetary policy divergence between major central banks. Historical one-month volatility for EUR/USD has dropped sharply in March to its lowest level since November 2021 as it continues to move back closer to the pre-COVID crisis lows from in early 2020. The dovish shift in BoE policy guidance after last week’s MPC meeting has resulted in market expectations for the start of monetary easing cycles of major central banks becoming even more aligned. The BoE, ECB and Fed are now all expected to begin cutting rates in June. The UK rate market is pricing in 16bps of cuts by the BoE’s policy meeting on 20th June, the euro-zone rate market is pricing in 21bps of cuts by the ECB’s policy meeting on 6th June, and the US rate market is pricing in 19bps of cuts by the Fed’s policy meeting on 12th June. At the same time, market participants are expecting a similar amount of easing by the BoE, ECB and Fed through the rest of this year. All three major central banks are currently expected to deliver around three 25bps cuts by the end of this year. Current market expectations for a synchronized start to rate cut cycles from major central banks appear reasonable and favour further consolidation for the major FX pairs of EUR/USD, GBP/USD and EUR/GBP in the near-term. The main risk to that view would be if the Fed delays the start of their easing cycle in response to US inflation continuing to surprise to the upside at the start of this year which would encourage a stronger US dollar.

KEY RELEASES AND EVENTS

|

Country |

GMT |

Indicator/Event |

Period |

Consensus |

Previous |

Mkt Moving |

|

CA |

12:15 |

BoC Senior Deputy Governor Rogers Speaks |

-- |

-- |

-- |

!! |

|

US |

12:30 |

Durable Goods Orders (MoM) |

Feb |

1.2% |

-6.1% |

!! |

|

US |

13:00 |

S&P/CS HPI Composite - 20 s.a. (MoM) |

Jan |

-- |

0.2% |

! |

|

US |

14:00 |

CB Consumer Confidence |

Mar |

106.9 |

106.7 |

!!! |

|

US |

16:30 |

Atlanta Fed GDPNow |

Q1 |

2.1% |

2.1% |

!! |

|

EC |

19:00 |

ECB's Lane Speaks |

-- |

-- |

-- |

!! |

Source: Bloomberg